Now that your business is going gangbusters, let’s take a look at your corporate investments. I’m talking about your active business income that has not been paid out in taxes or distributed to shareholders. Since that amount can be significant ($85,000 for every $100,000 of active business income in Ontario), it may not take long before you’ve accumulated significant chunks of change in your corporate account. Let’s put that lazy money to work!

As a responsible steward of your corporate investments, you probably won’t want to get too wild and crazy. So let’s say you invest your corporate cash in a sturdy Canadian bond ETF, and after a year you’ve already received $10,000 of Canadian interest income.

Now what? No big surprise: You’ll pay taxes on this passive income by declaring it on your corporate tax return. How does that work?

There are a number of similarities – as well as some notable differences – between how your corporation’s active business income and passive income are taxed. In the example below, I’ve illustrated the tax impact of $10,000 of Canadian interest income earned within a corporation. This aggregate investment income can be found on Schedule 7 of the corporate tax return.

Source: Corporate Taxprep – Schedule 7 (2016)

A work of ART

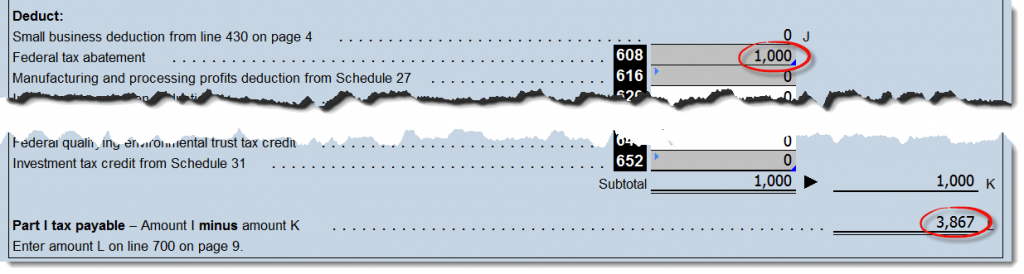

For starters, your corporation is taxed the same basic federal rate of 38%, whether it’s on your active business income or on passive Canadian interest income. In our example, $10,000 × 38% = $3,800.

But unlike for the active business income, your corporation also pays an additional refundable tax on investment income (ART) of 10 2/3% (or 10.67%) on the Canadian interest income. In our example, that’s an additional $10,000 × 10.67% = $1,067.

Source: Corporate Taxprep – T2 Corporation Income Tax Return (2016)

As with active business income, the federal tax abatement reduces the basic federal tax rate by 10%, which is intended to approximately offset the taxes levied by the province. In our example, that’s $10,000 × 10% = $1,000.

If we take the basic federal taxes of 38%, include the additional refundable tax of 10.67%, and deduct the federal tax abatement of 10%, we end up with federal Part I tax payable of 38.67%, or $3,867 in our example.

Of the 38.67% of federal Part I tax payable, 8% is considered non-refundable, while 30.67% is refundable when taxable dividends are paid to shareholders. (More on that in my next blog post.)

Source: Corporate Taxprep – T2 Corporation Income Tax Return (2016)

Size doesn’t matter

You may have noticed there’s no small business deduction in the tax calculations above. That’s because our federal government wants to encourage small business owners to invest mostly in their active businesses instead of in passive ETF portfolios.

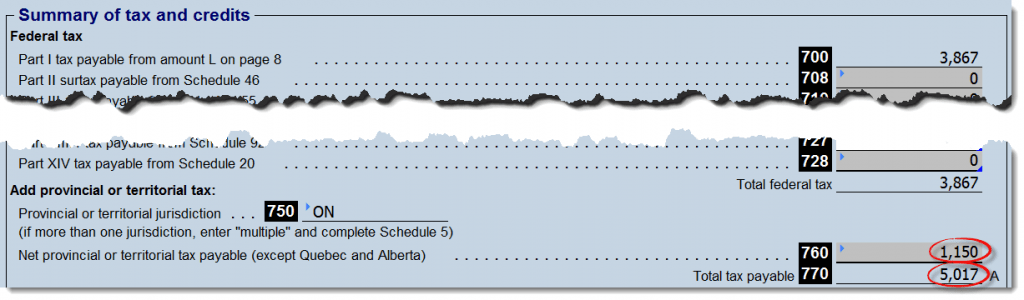

The provincial and territorial governments feel the same way, and offer no deduction for small business owners’ passive investments. Ontario levies the full tax rate of 11.5% on Canadian interest income, instead of the reduced 4.5% rate eligible small businesses incur on their active business income. This full pop amounts to $10,000 × 11.5% = $1,150 in our example.

Once we total the federal and provincial taxes, we end up with total taxes payable of 50.17%, or $5,017 in our example.

Source: Corporate Taxprep – T2 Corporation Income Tax Return (2016)

The taxes on corporate investments are significant, but your company is still left with an extra $4,983 it wouldn’t otherwise have if the cash were left to languish. I’ve included a summary of the results in the chart below.

Next up, you may now be wondering how you get back those refundable taxes. Great question. We’ll look at that in my next blog post which will discuss the dividend refund.

Corporate Taxation: $10,000 of Canadian Interest Income

| General Formula | Amount | Calculation |

|---|---|---|

| Base amount of Part I tax | $3,800 | $10,000 × 38% |

| Add: Additional refundable tax on investment income (ART) | $1,067 | $10,000 × 10.67% |

| Deduct: Federal tax abatement | ($1,000) | $10,000 × 10% |

| Equals: Part I tax payable | $3,867 | $3,800 + $1,067 - $1,000 |

| Add: Provincial or territorial tax | $1,150 | $10,000 × 11.5% (Ontario) |

| Equals: Total tax payable | $5,017 | $3,867 + $1,150 |

| Equals: After-tax corporate income | $4,983 | $10,000 - $5,017 |

Hi Justin,

Thanks for the posts, they’re very informative.

What is your recommendation regrading the ideal bond ETF to hold in a corporate investment account?

I have run out of ‘room’ for bonds in my RRSP, TFSA (all holding ZAG) and now need to start to hold bonds in the

corp, to maintain my 65:35 asset allocation. Retirement is 25 years away, and I am comfortable with ETF’s

or GIC’s. I’ve read your post on the BMO discount bond ETF.

Thanks very much,

Jamie

@Jamie Brown: If you’re looking for short-term fixed income exposure (i.e. 3-year average maturity), then a ladder of 1-5 year GICs or the First Asset 1-5 Year Laddered Government Strip Bond Index ETF (BXF) are likely your most tax-efficient options. If you’re looking for broad-market fixed income exposure (i.e. 10-year average maturity), then the BMO Discount Bond Index ETF (ZDB) is expected to be more tax-efficient than most plain-vanilla bond ETFs. If you’re comfortable with swap-based ETFs, the Horizons CDN Select Universe Bond ETF (HBB) is likely the most tax-efficient option (as all returns are considered to be deferred capital gains).

Very educational post (at least for me). To my surprise: income from bond ETF is considered as an interest and not a dividend. It’s not an issue for my Canadian investment, since the banks are reporting it via the T-3 and T-5, but I have Canadian bond ETFs outside of Canada which I have to report by myself. Many thanks

@Jerry: Canadian bond ETF distributions are generally a combination of interest, capital gains and return of capital. In order to obtain the accurate distribution breakdown for your bond ETFs, I would recommend visiting http://www.cds.ca and using their tax breakdown service.

After a few months of worrying what Mr. Trudo and Morneau are cooking for the “rich” we finally heard something positive from you Justin to make some of usfeel a little positive about the fate of professional corporations. Thanks for your positivity and hopefulness !looking forward for some more posts

@Costas: You’re very welcome – thanks for reading :)

Nice post Justin – look forward to future posts on the subject and the proposed changes.

@Matt: Thanks for the feedback! Did you just start investing within your corporation, or have you been doing it for awhile?

great post again Justin, to bad timing on these posts with Morneau’s announcement yesterday re: passive investment inside corp

would love to hear your take on that as well

@Tim: I’m glad you’re enjoying the posts (there’s many more of them in the works).

In terms of Morneau’s recent announcement, I would argue that this is the ideal time to be writing on this topic. The changes are not going to be retroactive, which means that many investors will still have significant corporate accounts to invest within, as well as personal non-registered accounts. It is now more important than ever to understand the tax implications of the various types of investment income. I’m very excited to be releasing more information on this topic in the future that should help investors save taxes! :)