Aren’t GPS devices the best thing ever? You punch in your desired destination and they tell you exactly where to go. Then again, every so often, they’ll go wonky on you, insisting you turn on a street that doesn’t even exist, or sending you straight into a major traffic jam.

Just so with implementing asset location, as introduced in my last post. General guidelines can be useful when trying to understand complicated topics like tax-efficient investing. In practice, however, these rules of thumb can lead you astray – especially if you follow them blindly, without regard to what’s going on right around you.

For example, you’ll often hear that it’s wise to fill up your taxable accounts with Canadian equities first and global equities next. Sometimes, this makes sense, as the Canadian company dividends receive preferential tax treatment (and global stock dividends don’t).

But where do you live? Depending on your actual tax rate and which province or territory you call home, there may be times when this “Canada first” rule of thumb might be a thumbs-down idea for you.

Today, I’ll explain how to estimate the taxable dividends on the equity ETFs in my model portfolios. We’ll then review the taxes payable in 2016 on each of the ETFs for residents across Canada. I’ll wrap up with suggested taxable account asset locations for top-rate taxpayers in each jurisdiction.

By the way, all yields and MERs below are annual; I’ll skip repeating that every time!

Canadian Equities

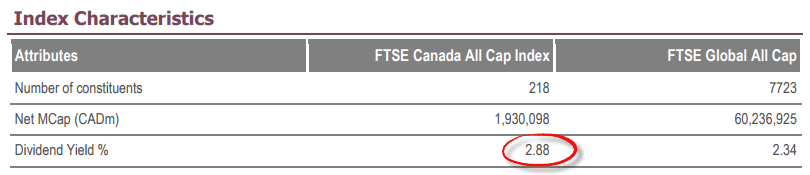

The Vanguard FTSE Canada All Cap Index ETF (VCN) follows the FTSE Canada All Cap Index, which has a gross dividend yield of 2.88%. Once we deduct the fund’s MER of 0.06%, we end up with a taxable dividend yield of 2.82%. Although this may seem high relative to the other asset classes below, you’ll recall that the eligible dividends receive preferable tax treatment, resulting in lower taxes than if the dividends were treated as ordinary income.

So … remember that rule of thumb, suggesting higher-income earners should first hold Canadian equities in their taxable accounts before all other asset classes? This really only applies in jurisdictions with relatively low eligible dividend tax rates (generally below 35%). Otherwise, you may be better off first holding certain foreign equities in your taxable accounts, even though their dividends are fully taxable as income.

Source: FTSE Russell Index Fact Sheet as of July 31, 2017

U.S. Equities

The iShares Core S&P U.S. Total Market Index ETF (XUU) follows the S&P Total Market Index, which has a measly gross dividend yield of only 1.90%. After deducting the fund’s expenses of 0.07%, the taxable dividend yield drops to about 1.83%. Even though taxes are initially withheld on the foreign dividends, they are generally recoverable at tax time, when you will be fully taxed on the dividends after the fund’s expenses have been deducted.

For provinces or territories with relatively high eligible dividend tax rates (i.e. above 35%), U.S. equities may be a more tax-efficient first choice to hold in your taxable accounts, instead of the Canadian-first rule of thumb.

Source: S&P Dow Jones Index Fact Sheet as of July 31, 2017

International Equities

The iShares Core MSCI EAFE IMI Index ETF (XEF) follows the MSCI EAFE IMI Index, which boasts an impressive dividend yield of 2.96%. As XEF holds the underlying stocks directly, any foreign withholding taxes are generally recoverable at tax time. Similar to U.S. equities, investors will be fully taxed on the gross dividends after deducting the product fees of 0.22%, for a taxable dividend yield of about 2.74%.

Although many investors love their dividends, this spells trouble for taxable investors throughout Canada. As I mentioned in my last blog post, if you’re going to hold any equities in your RRSP accounts, international equities should be your first choice (and your last choice for taxable accounts). This is one rule of thumb that applies nationwide, since there is not a single province or territory where holding international equities in taxable accounts first is expected to reduce the tax bill.

Source: MSCI Index Fact Sheet as of July 31, 2017

Emerging Markets Equities

The iShares Core MSCI Emerging Markets IMI Index ETF (XEC) follows the MSCI Emerging Markets IMI Index. With a gross dividend yield of 2.32%, it falls somewhere between U.S. and international equities.

As XEC doesn’t hold the underlying stocks directly, there’s one layer of unrecoverable foreign withholding taxes, with an estimated tax drag of 0.23%.

With fees of 0.26%, it’s also the most expensive ETF in my model portfolios. After deducting the fees and foreign withholding taxes, we end up with a taxable dividend yield of about 1.83% (which happens to be identical to the U.S. equity taxable dividend yield). This low yield may make emerging market equities even more tax-efficient than Canadian equities in many jurisdictions going forward (including Ontario, Manitoba, Quebec and Nunavut).

Source: MSCI Index Fact Sheet as of July 31, 2017

Our Model Portfolio Summary

So, in summary, below is the expected taxable dividend yields on the ETFs in my model portfolios. (Remember, VCN’s dividend yield is taxed at the lower eligible dividend tax rate, while the remaining ETFs are taxed at ordinary income tax rates.)

Expected Taxable ETF Dividend Yields

| Exchange-Traded Fund | Gross Dividend Yield | Unrecoverable Foreign Withholding Tax | Management Expense Ratio (MER) | Taxable Dividend Yield |

|---|---|---|---|---|

| Vanguard FTSE Canada All Cap Index ETF (VCN) | 2.88% | - | (0.06%) | 2.82% |

| iShares Core S&P U.S. Total Market Index ETF (XUU) | 1.90% | - | (0.07%) | 1.83% |

| iShares Core MSCI EAFE IMI Index ETF (XEF) | 2.96% | - | (0.22%) | 2.74% |

| iShares Core MSCI Emerging Markets IMI Index ETF (XEC) | 2.32% | (0.23%) | (0.26%) | 1.83% |

Sources: FTSE Russell, S&P Dow Jones and MSCI Index Fact Sheets as of July 31, 2017. BlackRock Canada and Vanguard Canada.

Going Local

Now, to the good stuff. What are the optimal asset location guidelines where you live?

For that, let’s estimate which asset class has the lowest expected annual tax liability in each province or territory by calculating 2016 taxes payable on a $10,000 investment for a taxpayer in the highest marginal tax bracket.

To make the comparison a little easier on the eyes, I’ve included a second chart below that provides the optimal 2016 asset location order for taxable accounts. (I’ve only considered annual income and its tax ramifications here, since we cannot accurately predict your unique long-term, unrealized gains.)

The compelling conclusions?

- Most of the provinces and territories with the lowest eligible dividend tax rates tend to favour Canadian equities first (except Nunavut, which has relatively low ordinary income and low eligible dividend tax rates)

- Jurisdictions with the highest eligible dividend tax rates favour U.S. equities first.

- Throughout Canada, international equities place dead last in terms of tax-efficiency (due to the relatively high taxable dividend yield).

- Going forward, emerging markets may swap places with Canadian equities in Manitoba, Nunavut, Ontario and Quebec.

2016 taxes payable on a $10,000 investment (top marginal tax bracket)

| Province or Territory | Vanguard FTSE Canada All Cap Index ETF (VCN) | iShares Core S&P U.S. Total Market Index ETF (XUU) | iShares Core MSCI EAFE IMI Index ETF (XEF) | iShares Core MSCI Emerging Markets IMI Index ETF (XEC) |

|---|---|---|---|---|

| Alberta | $88 | $93 | $131 | $101 |

| British Columbia | $87 | $92 | $130 | $100 |

| New Brunswick | $95 | $103 | $145 | $112 |

| Northwest Territories | $79 | $91 | $128 | $99 |

| Prince Edward Island | $95 | $99 | $140 | $108 |

| Saskatchewan | $84 | $93 | $131 | $101 |

| Yukon | $69 | $93 | $131 | $101 |

| Manitoba | $105 | $97 | $138 | $106 |

| Nunavut | $92 | $86 | $121 | $93 |

| Ontario | $109 | $103 | $146 | $112 |

| Quebec | $111 | $103 | $145 | $112 |

| Newfoundland and Labrador | $113 | $96 | $136 | $105 |

| Nova Scotia | $116 | $104 | $147 | $113 |

Sources: 2016 Personal TaxPrep, TaxTips.ca, CDS Innovations Tax Breakdown Service, BlackRock Canada, Vanguard Canada

2016 Asset Location Order for Taxable Accounts

| Province or Territory | Ordinary income (top marginal tax rate) | Eligible dividends (top marginal tax rate) | 1st | 2nd | 3rd | 4th |

|---|---|---|---|---|---|---|

| Alberta | 48.00% | 31.71% | Canadian Equities | U.S. Equities | Emerging Markets Equities | International Equities |

| British Columbia | 47.70% | 31.30% | Canadian Equities | U.S. Equities | Emerging Markets Equities | International Equities |

| New Brunswick | 53.30% | 34.20% | Canadian Equities | U.S. Equities | Emerging Markets Equities | International Equities |

| Northwest Territories | 47.05% | 28.33% | Canadian Equities | U.S. Equities | Emerging Markets Equities | International Equities |

| Prince Edward Island | 51.37% | 34.22% | Canadian Equities | U.S. Equities | Emerging Markets Equities | International Equities |

| Saskatchewan | 48.00% | 30.33% | Canadian Equities | U.S. Equities | Emerging Markets Equities | International Equities |

| Yukon | 48.00% | 24.81% | Canadian Equities | U.S. Equities | Emerging Markets Equities | International Equities |

| Manitoba | 50.40% | 37.78% | U.S. Equities | Canadian Equities | Emerging Markets Equities | International Equities |

| Nunavut | 44.50% | 33.08% | U.S. Equities | Canadian Equities | Emerging Markets Equities | International Equities |

| Ontario | 53.53% | 39.34% | U.S. Equities | Canadian Equities | Emerging Markets Equities | International Equities |

| Quebec | 53.31% | 39.83% | U.S. Equities | Canadian Equities | Emerging Markets Equities | International Equities |

| Newfoundland and Labrador | 49.80% | 40.54% | U.S. Equities | Emerging Markets Equities | Canadian Equities | International Equities |

| Nova Scotia | 54.00% | 41.58% | U.S. Equities | Emerging Markets Equities | Canadian Equities | International Equities |

Sources: 2016 Personal TaxPrep, TaxTips.ca, CDS Innovations Tax Breakdown Service, BlackRock Canada, Vanguard Canada

So, there you have it: A few jurisdiction-specific rules of thumb to guide you along your tax-wise way. But, as with that GPS that usually takes you where you want go, you may want to take a good look around at your personal circumstances before blindly following anyone’s general directions – even mine.

I’ve been spending quite a bit of time lately on both asset location as well as foreign WHT and have found your blog posts and some of the white papers very helpful. In one post, you suggest that DIY investors should hold the same asset mix (e.g. 60/40) in each account type to avoid ending up with a more aggressive after tax portfolio than desired (and to avoid the headache of optimizing your after tax portfolio for what could be a fairly small benefit). That all makes sense to me, however I’m wondering whether it still makes sense to optimize the equity portion of the portfolio. As a simple example, if you had a portfolio that was split evenly across an RRSP, TFSA and Taxable account (adjusting for the tax impact of the RRSP), would it make sense to make your taxable account 60% Canadian Equity / 40% Fixed Income; your TFSA 60% International Equity / 40% Fixed Income and your RRSP 60% US Equity (Using US Funds) / 40% Fixed Income? I’m in Alberta so on the lower end of eligible dividend rates relative to other provinces. Thanks!

@Jeff: I’ve written about these asset location strategies in great detail (and have also covered them on the CPM Podcast):

https://canadianportfoliomanagerblog.com/canadian-portfolio-manager-introducing-the-ludicrous-etf-portfolios/

https://canadianportfoliomanagerblog.com/canadian-portfolio-manager-introducing-the-plaid-etf-portfolios/

Hey Justin,

Thanks for the post. I really liked the asset location order table. I am wondering if you have something similar for RRSPs and TFSAs.

From your other posts, this is what I came up with:

RRSP: 1) US 2) Emerging 3) International 4) Canadian <– using US-listed for US/Emerging/International

TFSA: 1) Canadian 2) US/International (tie) 3) Emerging <– using Canadian-listed ETFs

Do you agree?

Thanks

@Pete: There are many ways to look at asset location decisions. From a foreign withholding tax perspective (for just a TFSA and RRSP), I would likely arrange them in the following order:

RRSP: 1) Emerging 2) US 3) International 4) Canadian <– using US-listed for US/Emerging/International TFSA: 1) Canadian 2) International 3) US 4) Emerging <– using Canadian-listed ETFs

Thanks for the quick reply. Can you elaborate on what other factors I should consider?

@Pete: To reduce foreign withholding taxes:

– Canadian equities should go in the TFSA first (as there are no withholding tax implications, whereas U.S., international and EM all have a tax drag).

– International equities should go next (a Canadian-listed ETF that holds the international stocks directly) – whether you hold this asset class in an TFSA, or a U.S.-listed international equity ETF in your RRSP, the withholding tax implications are the same

– U.S. equities should go in the TFSA next, as the withholding tax drag is less than most emerging markets equity ETFs (like XEC or VEE).

– Emerging markets equity ETFs should go in the TFSA last.

– Reverse the rules for the RRSP

Sorry, I don’t think I was clear in my followup question. In your first reply, you said “There are many ways to look at asset location decisions. From a foreign withholding tax perspective (…)”, so I understood that there are factors besides FWT to guide an asset location decision. I was wondering what these factors are.

The bottom of this site https://www.savespendsplurge.com/investing-series-where-to-hold-what-funds-in-your-retirement-accounts-for-maximum-tax-efficiency-canada/ says that we have to submit a W8-BEN form or Canadian ID to your discount brokerage to lower dividend taxes from 30% to 15%. Is that true? I thought this was done automatically if you’re Canadian.

@SD: I would contact your specific brokerage to determine whether they need you to complete the W8-BEN form. If you’re holding U.S.-listed ETFs in your accounts, you should be able to determine the withholding tax rate that is being applied by reviewing your account statements (if it’s 30%, you should definitely follow-up with your brokerage).

Is there situations where we use non-eligible dividend tax rate instead ordinary income tax rate to find out how much taxes we pay on dividends ?

@Sebastian: If you’re calculating investment income which is distributed from your corporation to you personally in the form of an ineligible dividend, then you would need to use the applicable ineligible dividend tax rate (and also include the corporate taxes originally payable on the investment income, minus the refundable corporate taxes when the cash is distributed to you personally).

Hi Justin, this is a super helpful post, so thank you.. For an Ontario resident who doesn’t wasn’t to break XAW up into 3 ETFs, am I correct in thinking they should hold their Canadian equity ETF in the taxable account before holding XAW?

And how solid will that likely hold in the future? Tax rates and dividend rates change (and one might even move to a different province and end up changing jurisdictions), I’m wondering if it might be a wise strategy to hold the same geographic allocation in both taxable and non taxable accounts. I know you can’t provide specific advice, but I’d be interested in your thoughts. Also for a taxable account vs a TFSA, if one does decide not to hold the same geographic allocation in both of these accounts, is after tax allocation a concern? Thanks!

@Robert: As you said, without knowing future tax rates, returns, dividend yields, etc., holding the same asset allocation across accounts is a reasonable strategy.

If you decide to hold more equities in your TFSA (relative to your taxable account), I don’t think this is something to be too concerned about (just understand that you are taking slightly more risk from an after-tax standpoint, but you’ll never really notice from a behavioural perspective).

Thank you so much for all your information. But there’s so much to wrap my head around! So to clarify, this only applies to ETFs that are paying dividends. This does not apply if using swap-based ETFs, correct? I’m trying to decide whether to use swap-based or not, so trying to understand the tax implications of each. Thanks!

@Rozalyn Allan: That’s correct – if you’re using swap-based ETFs, they do not pay dividends.

Hi Justin, I really enjoy your blog as I learn so much.

I am trying to understand how to obtain your results. From what I understand, here is formula you may have used:

VCN: (Gross Dividend Yield – Management Expense Ratio) x Eligible dividends rate

XEF: (Gross Dividend Yield – Management Expense Ratio) x Ordinary income

XEC: (Gross Dividend Yield – Management Expense Ratio) x Ordinary income

What is the formula for XUU? I thought it would be like XEF and XEC, but it doesn’t seem to be. It looks like it is (Gross Dividend Yield x Ordinary income), but I don’t understand why we would not subtracts the MER in this case.

Thank you for your time.

@Sebastien: The results are actual figures from the 2016 tax year (I used the CDS tax breakdown service to determine the exact distribution amounts and income types). The estimates are forward looking figures using current dividend yields and MERs.

I understand, but why did you use the formula [Gross Dividend Yield x Ordinary income] instead of [(Gross Dividend Yield – Management Expense Ratio) x Ordinary income] to determine the estimated taxes for XUU? Is this a mistake?

@Sebastien: I’m not using this formula for XUU – why do you feel that I am?

The reason why I feel that you’re is because I don’t get the same results as yours if I use the taxable dividend yield. For XUU, I need to use the gross dividend yield to find the same results.

Maybe I am wrong, but I think the result for Alberta should be (1,90% – 0,07%) x 48% = about $88. But you results seems to be 1,90% x 48% = about $91. The rounding can explain a $2 difference with your result of $93.

I try to understand how I can find the right values with your numbers so I can do it with any other ETF. Any help would be greatly appreciated.

@Sebastien: The calculations are based on actual T3 ETF data for the 2016 tax year (so you would need to download the tax breakdowns from CDS Innovations).

The process for estimating the tax impact going forward would be to use the current gross dividend yield from the index fact sheets, subtract the MER, and then multiply the figure by your marginal tax rate.

Sorry, English is not my first language and I misunderstood what you said earlier. I now understand that the taxable dividend yields in this article are from July 31th, 2017 so I can’t use them to find the taxes payable for year 2016.

Thank you for the informations. It is great help for me.

@Sebastien: Perfect – I’m glad this makes more sense now :)

Justin,

do these rules hold true for mutual funds diversified into different asset classes denominated in CAD$?

@Marc: For actively managed mutual funds, I can’t say for certain whether these rules would hold (as the manager may be purchasing stocks with higher or lower dividend yields than the broad stock market).

@ Justin @ Pascale Courrieu @ Kevin

+1 for an article on order of withdrawal between RRSP, TFSA, and Taxable in retirement.

+2 for an article on order of withdrawal between RRSP, TFSA, and Taxable in retirement.

Hi Justin

Looking forward to this article as well . Could you include in your article a possible incorporation with the Rebalancing Tool?

Thanks

Wayne

@Kevin, @Justin:

+1 for an article on order of withdrawal between RRSP, TFSA, and Taxable in retirement.

Hi Justin,

Love you blog. Can you do an article on order of withdrawal between RRSP, TFSA, and Taxable in retirement. there are a few online but they are very general.

Thanks

Kevin

@Kevin: Thanks for the feedback! That does sound like an interesting topic – I’ll see what I can put together in a future blog post.

Love this post Justin. Helps confirm everything that you and Dan have always taught, but with even more detail. What would Canadian investors do without you two?! Keep up the great work. It’s needed and very much appreciated.

@Chrissy: I’m so glad you’ve enjoyed reading our work – there’s many more articles in the works :)

Hi Justin,

As a resident of Ontario who has maxed out my tfsa and rrsp contribution room, I have trouble accepting the idea that booting U.S. equities from my tax advantaged accounts is ultimately a fiscally responsible thing to do.

I want my tfsa and rrsp to grow to be as big as possible so that when I retire (or need to make a big purchase) I can draw as much tax free/deferred money as possible. Taking my American index fund, which arguably has the highest growth potential of all my funds, out of these accounts to save a few bucks on my present day tax bill seems a little penny wise and pound foolish. However, this is more of a hunch on my part, I know we cannot predict future returns, and I am not sure if I am making this out to be a bigger issue than it is.

Any help/thoughts would be greatly appreciated.

Thanks

Chuck

@Chuck: Which asset class would you prefer to hold in your taxable accounts first? For an Ontario taxpayer, the annual taxes payable are expected to be very similar for all assets classes (even if US equities come out slightly ahead), so I don’t see any issues with choosing a different equity asset class for your taxable account if you prefer.

Whether you should hold fixed income instead of equities in your taxable account first also has some merit, depending on your personal circumstances. For example, if you will be retiring shortly and are planning to withdraw from your taxable account first, you may prefer to hold a ladder of GICs in the taxable account first so that you do not have to realize any gains as you withdraw from the portfolio.

I will also be writing some posts over the next couple of months on when it makes sense to hold fixed income in your taxable account first instead of equities.

Awesome post.

How does this change if we are holding the US listed version of US Equities within an RRSP to prevent the withholding tax? I’ve seen it recommended to hold US equities in an RRSP, would the lower dividend yield on US Equities change this as well?

@Ryan: I’m not sure I understand your question as it relates to this blog post – would you mind elaborating a bit more? Thanks!

I think you’re right, i’m not sure it would have an impact on this post.

I was just wondering/thinking about the withholding tax on US equities, and if that would impact this decision as well. http://canadiancouchpotato.com/2013/12/09/ask-the-spud-when-should-i-use-us-listed-etfs/

After reading more, I think the withholding tax might actually further support the idea of putting US equities into taxable accounts.

Thanks!

Thanks Justin for this very good analysis. One questions though. You indicate that in jurisdictions with the highest eligible dividend tax rates, one should favour US equities first because you pay less taxes. However, the US equity dividend yield is roughly 1% less than the Canadian equity yield. Isn’t normal to pay less taxes if you have less dividend? On a per received dollar basis, wouldn’t you end-up paying 39 to 41% taxes for Canadian dividend VS 53-54% on US dividend in the last four provinces, still providing a small advantage for Canadian dividend? Or maybe there is something I don’t get.

Thanks for clarifying,

Pascal

@Pascal Marcoux: The ultimate dollar amount of taxes you pay on your Canadian vs. US equities should be the focus (not just the difference in tax rates on the investment income). Even though Canadian eligible dividends are taxed more favourable, the higher dividend yield takes away some of this benefit (resulting in a similar tax liability to US equities in some jurisdictions).

Hi Justin,

Thanks for the great post. Indeed, there is so much dogma that is adhered to. To add a a further layer of personalization, one has to consider the tax bracket that they are in, as the results will change with this as well. This of course adds a layer of complexity to the post. One way around this is to compare the top income bracket to the lowest, rather than each bracket. This is a more realistic scenario for many retirees.

People, and sites, rarely consider after-tax performance of our returns and we rarely see posts such as this.

Great post.

@Kulvir: Thanks! Great point about the individual’s tax bracket having an impact on the results. I wanted to include a separate analysis (similar to what you had described), but the blog post was already becoming quite lengthy – so I just decided to add a few caveats along the way.

Hello Justin, I want to add my thanks and appreciation as well. Amazing post!

I took for granted that Canadian Equities should have priority in taxable accounts vs. other type of equities because of the canadian dividend tax credit.

I know understand that eligible dividend tax rate and the equity dividend tax yield are what should help in the decision for asset location (with a few other considérations that you point out).

@Philippe V: Thank you for your feedback – I’m glad to hear you enjoyed the post :)

Fantastic post, Justin. Thank you for sharing this information!

@Bruno: You’re very welcome! :)