It’s finally here! While many Canadians were gearing up for the much anticipated iPhone 6 launch, I was patiently awaiting an upcoming portfolio management software release: the PWL Tax Loss Selling Report.

PWL advisors can now generate a report that shows all non-registered client accounts that have unrealized capital losses. Any capital losses realized must first be used to offset capital gains realized in the current tax year; they can then be carried back up to three years (or carried forward indefinitely). This allows investors in relatively high marginal tax brackets to defer taxes and possibly realize them at a more advantageous time.

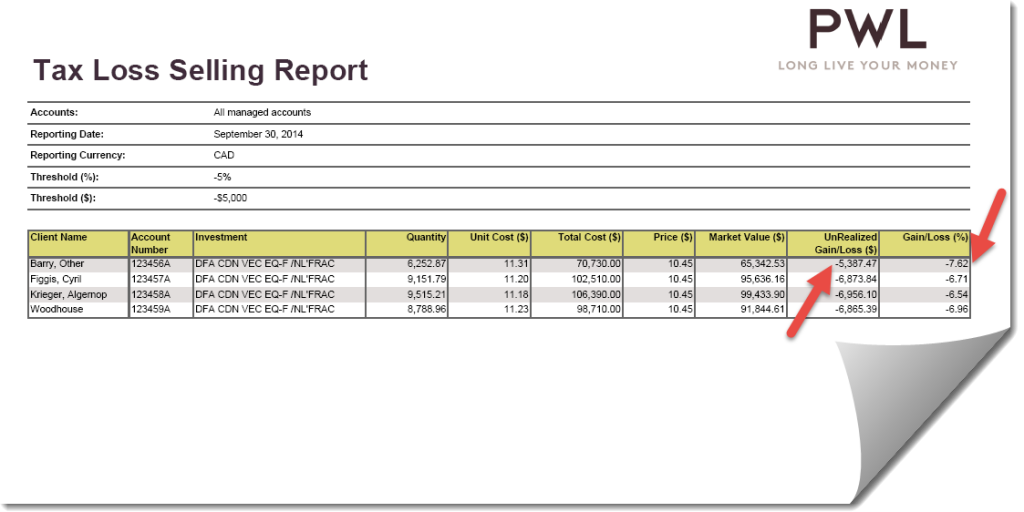

The report was inspired by Larry Swedroe’s tax loss selling rule of thumb. His rule states that an investor should consider realizing a loss if it is at least $5,000 and at least 5% of the book value.

For example, suppose Other Barry purchased the DFA Canadian Vector Equity Fund Class F (DFA600) for $70,730. On September 30, 2014, the fund had dropped in value to $65,342.53 (resulting in an unrealized capital loss of $5,387.47). This loss represents a 7.62% drop in the book value ($5,387.47 ÷ $70,730 = 7.62%). In this case, both of Swedroe’s tax loss selling thresholds have been met. The generated report will now include Mr. Barry’s holding as a potential tax loss selling candidate.

Source: PWL Capital

Know when to fold ‘em

The decision about whether to realize a capital loss depends on the investor’s particular tax situation (my colleague, Dan Bortolotti, wrote about this topic in a recent blog). Once the decision has been made to realize the loss, a replacement security must be chosen (in order to maintain similar market exposure). I would encourage advisors and DIY investors to have a tax loss selling plan in place prior to implementing their portfolios.

I’ve included the tax loss selling pairs below that we use with our PWL clients, as well as the monthly tracking errors of the underlying indices. As discussed in our white paper, Tax Loss Selling, tracking error is the standard deviation of the differences in the monthly returns of the underlying indices. A low value indicates that the indexes have tracked each other closely in the past.

Tax Loss Selling Pairs and Monthly Tracking Errors of Indices: 01/2004-12/2013

| Initial Fund | Replacement Fund | Monthly Tracking Error |

| DFA Canadian Vector Equity Fund Class F (DFA600) Dimensional Canadian Vector Equity Index | DFA Canadian Core Equity Fund Class F (DFA256) Dimensional Canadian Core Equity Index | 0.364 |

| Vanguard FTSE Canada All Cap Index ETF (VCN) FTSE Canada All Cap Index | iShares Core S&P/TSX Capped Composite Index ETF (XIC) S&P/TSX Capped Composite Index | 0.326 |

| DFA US Vector Equity Fund Class F (DFA223) Dimensional US Vector Equity Index | DFA US Core Equity Fund Class F (DFA293) Dimensional US Core Equity Index | 0.772 |

| Vanguard Total Stock Market ETF (VTI) CRSP US Total Market Index | iShares Russell 3000 ETF (IWV) Russell 3000 Index | 0.106 |

| DFA International Vector Equity Fund Class F (DFA227) Dimensional International Vector Equity Index | DFA International Core Equity Fund Class F (DFA295) Dimensional International Core Equity Index | 0.347 |

| Vanguard Total International Stock ETF (VXUS) FTSE Global All Cap ex US Index | iShares Core MSCI Total International Stock ETF (IXUS)MSCI ACWI ex USA IMI | 0.386 |

Sources: BlackRock, CRSP, FTSE, MSCI, Russell Investments, Vanguard Group, Morningstar Direct, Dimensional Returns 2.0

Suppose the advisor decides to realize the loss for Mr.Barry. He would place a trade to switch all units of the DFA Canadian Vector Equity Fund Class F (DFA600) to the DFA Canadian Core Equity Fund Class F (DFA256). The trade would settle on October 1 (trade date + 1 business days) and would need to be held for at least 30 days before it was switched back to the original holding (in order to avoid being deemed as a superficial loss). In this example, the replacement fund would need to be held by the investor from October 2 to October 31 (30 days). If the advisor switched back to the original fund on October 31, it would settle on November 3 (trade date + 1 business days), avoiding the superficial loss rules. ***Note: Most ETFs and stocks settle on T+3***

Hi Justin,

With yesterday’s market decline, I thought I had a tax-loss harvesting opportunity, but after reading your PWL white paper about tax-loss harvesting I think I might be subject to a superficial loss?

Suppose I held 10,000 shares of VEQT and paid $26 / share in my margin account. On Feb 28th 2020, I sold all my VEQT shares at $26.25 and bought XEQT. (e.g. I made a capital gain and no loss). Then, on March 9, the market tanked and my XEQT shares have dropped over 5% so I sold all XEQT shares and bought back VEQT.

Would this be considered a superficial loss by the CRA because of the transactions I had done on Feb 28 with VEQT/XEQT? ( e.g. because I held XEQT share in the 30 days prior to March 9th?)

If it is a superficial loss can I still sell all XEQT shares and purchase another security to avoid the superficial loss?

Thanks

@Guy Langevin: Good question. The ETF that you need to be concerned about is XEQT (it’s the one with the loss), so just focus on it. Did you buy any shares (other than the shares of XEQT that you sold at a loss on March 9) in the 30 days before, or the 30 days after? If the answer is no, you don’t have a superficial loss.

Yes, I bought 100 shares of XEQT on March 5 and 24 more shares on Mar 2.

During that period, I also held 2026 share of XFR from Dec 10, and sold XFR on Feb 28 (made a small capital loss of -$154.85). Not other transactions ( all distributions from XFR were paid in cash and no-drip)

Justin based on what you mentioned above, is this considered a partial superficial loss?

Thank you

Hi Justin,

I am starting a personal taxable account with my husband. We also have a CCPC.

I am using your taxable account portfolios of XAW, VCN and ZDB for both.

In terms of tax loss selling, would the personal taxable be treated separately from the CCPC?

That is, I can considered each account in silos without needing to sell the same ETF in both accounts simultaneously?

I do not hold these ETFs in my TFSA or RRSP. I hold VGRO on those accounts.

@Miwo: When tax loss selling in a personal account, you do need to consider your corporate account for superficial loss purposes:

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/personal-income/line-127-capital-gains/capital-losses-deductions/what-a-superficial-loss.html

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/personal-income/line-127-capital-gains/capital-losses-deductions/what-a-superficial-loss/affiliated-persons.html

Hi Justin,

That’s my concern! And my accountant thinks it’s okay. He said our CCPC is a different name and should be okay?

I will need to rethink my investments in the personal taxable account now.

Thanks for getting back to me!

Hi Justin,

Much thanks for the links. I understand this now. I even called my advisor and he was confused. Thankfully, my accountant was not.

I made a purchase within the 61-day window but I will NOT own shares 31 days following a sale that triggers a capital loss. For the superficial loss rule to apply, both of the conditions mentioned must be met.

Thanks again Justin!

@Dr. MB: You’ve understood it perfectly – well done! :)

Hi Justin,

I have bought multiple rounds of XAW in my Corporate Holdco Account between May 2018 up to Oct 1, 2018.

As you can see, the market has handed a good discount. I would like to sell for tax loss selling but am confused about the 30 days before the selling. And Oct 1, 2018 would fall within that.

If I can sell for a loss, I’d love to know. I plan to buy more of my ex Cdn etf soon. But not sure if I can tax loss sell the XAW and then go buy the VXC

I only hold these ETFs in my Corp Holdco.

Good grief you are an amazing help!!

Hi Justin,

I am using your model portfolio for my CCPC. I am planning to tax loss sell some XAW which fulfills the criteria for >5K and >5% as Mr. Swedroe advised. Are the tax loss pairs still XAW to VXC and VCN to XIC?

@Dr. MB: XAW to VXC is still my preferred choice. If VXC is showing a loss after 30 days, you may want to consider switching it back to XAW, as it is slightly more tax-efficient (XAW holds the underlying international stocks directly, avoiding a layer of foreign withholding tax).

VCN to XIC is my preferred choice. VCN to ZCN or TTP also works. VCN to RCAN could also arguably be a possible pair (as RCAN follows the slightly different FTSE Canada All Cap Domestic Index). I doubt I would bother switching it back after 30 days (unless there was an additional $5,000 loss on XIC after 30 days).

Hello Justin,

I just bought some XAW on Oct 1, 2018 thus I am unable to tax loss sell this early. I also checked your updated ETF pairs report in 2016. I understand that you would run into the superficial loss rule if I had bought the same ETF 30 days before and 30 days after the date sold it.

Thanks again for all your information. It is hugely appreciated.

@Dr. MB: If you bought the shares of XAW in your corporate account on October 1, 2018 (and in no other affiliated account), you can still sell all of the existing shares of XAW now and realize the loss. For the superficial loss rule to apply, you must also hold the shares of XAW within 30 days after the sale, which you wouldn’t be doing.

When Shares are Fully Sold Quickly After Being Purchased:

https://www.adjustedcostbase.ca/blog/what-is-the-superficial-loss-rule/

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/personal-income/line-127-capital-gains/capital-losses-deductions/what-a-superficial-loss.html

Hi Justin,

I have been reading about tax-loss harvesting, but I have never quite understood the real benefit. It seems you are simply deferring the tax that will inevitably be paid.

However, if I am not mistaken, after considering it again, does the benefit arrive under the following circumstance: You defer capital gains in a year you are in a high tax bracket by harvesting losses, and then ideally when you actually do realize the gains you are in a lower bracket. Is it sort of like an RRSP in this way? The true benefit, assuming tax brackets stay the same, is that you are trying to realize the gain and pay taxes on it when you are in a lower bracket? Does this also mean that tax-loss harvesting is only useful in non-registered accounts?

@Nik – tax loss selling is only relevant for non-registered accounts. The benefit that you mentioned (realizing the gains in a future lower income year), may be possible (and would lead to higher after-tax returns). Another benefit would be to have an interest free loan from the government (which you could use to invest and continue compounding).