By now, you’ve likely been bombarded by articles – shelling out nearly as many opinions – on the government’s proposed tax changes for private corporations of all size. Remember that dividend refund “magic act” I covered? Guess what – that’s one of the tax breaks targeted for elimination. As you might imagine, this is causing quite a stir in the business community, with outcries ranging from “Government extortion!” to “It’s about freaking time!”

To inject some objectivity into the emotionally charged debates, let’s take a look at the numbers. Conclude what you will, and if you’d like to weigh in on the matter, the Department of Finance is inviting comments through October 2, 2017.

All’s fair in love, war … and tax codes

As I introduced in my dividend refund post, the federal government currently taxes 38.67% of a corporation’s passive interest income (plus provincial or territorial taxes). The corporation can then file for a 30.67% refund (with 8% non-refundable) once the taxable dividends are paid out to shareholders.

The government has proposed eliminating that refund entirely. Instead of just 8%, the entire 38.67% would become non-refundable.

What’s with the change in heart? Although the dividend refund mechanisms I described in my previous post allows integration to function reasonably well in theory (so everybody pays their fair tax share), it has tended to play out a little differently in reality. Small business owners are initially taxed at a much lower rate on their active business income than regular taxpayers incur on their personal income. In Ontario, the difference is 15% for small-business corporate taxes versus a top tax rate of 53.53% on personal taxes. This gives small businesses a big head start on the after-tax cash they’ve got left to invest in passive corporate investment portfolios. In industry jargon, they’re scoring an impressive tax deferral benefit.

To re-level the playing field, the government considered a few other ideas, but scrapped them as impractical for reasons I won’t inflict on you at this time. By settling on the current proposal – making all corporate taxes on passive investment income non-refundable – the goal is to make it a relatively moot tax point whether business owners invest their active business income in their corporate passive portfolio, or distribute the income to themselves (or other shareholders) for investing personally.

That’s the theory. Will it work in reality? Keep reading to see how the numbers compare. (And if you’re really a glutton for punishment, here’s a spreadsheet with the background calculations.)

Two’s company, three’s a crowd

In the example below, I’ve compared three taxpayers:

- An individual taxpayer

- A corporation taxed under the current (refund) system

- A corporation taxed under the proposed (non-refund) system

All three start with $100,000 of income that’s initially taxed at the top Ontario tax rate of 53.53% for the individual or the small-business tax rate of 15% for the corporations. The after-tax proceeds are then invested in portfolios earning 3% annual interest, taxed again, and then reinvested each year. The corporations pay 50.17% tax on their investment income each year, while the individual pays tax at 53.53%. At the end of 10 years, the corporations’ active business income and investment income is distributed to the business owners and taxed in their hands.

Starting portfolio (Ontario)

| Individual | Corporation: Current System | Corporation: Proposed System | |

|---|---|---|---|

| Income | $100,000 | $100,000 | $100,000 |

| Deduct: Combined federal/provincial personal or corporate tax | ($53,530) | ($15,000) | ($15,000) |

| Equals: Starting portfolio | $46,470 | $85,000 | $85,000 |

Sources: KPMG 2016 Personal Tax Rates, KPMG 2016 Corporate Tax Rates

On your marks … Get set … Get a head start

Under the current and proposed systems, the individual taxpayer’s starting portfolio is $38,530 less than either of the business owners’ portfolios ($85,000 – $46,470). The individual earns $1,394 of investment income in the first year ($46,470 × 3%) and pays $746 of federal/provincial taxes ($1,394 × 53.53%), leaving $648 of after-tax investment income after year-end ($1,394 – $746).

Both corporate portfolios earn $2,550 of interest in year one ($85,000 × 3%) and incur $1,279 in corporate taxes ($2,550 × 50.17%), leaving $1,271 of after-tax investment income ($2,550 – $1,279). The only difference is that the corporation under the current system designates $782 of the federal taxes as refundable ($2,550 × 30.67%), while the corporation under the proposed system makes no such distinction – all taxes are non-refundable.

Although this distinction initially makes no difference to the corporate taxes payable after year one ($1,279 either way), we’ll soon see how it paves the way for a dramatic impact on a business owner’s net worth once taxable dividends are distributed from the corporation to its shareholders after many years of investment growth.

After-tax investment income after 1 year (Ontario)

| Return on investment in year 1 | Individual | Corporation: Current System | Corporation: Proposed System |

|---|---|---|---|

| Starting portfolio | $46,470 | $85,000 | $85,000 |

| Earn: 3% interest | $1,394 | $2,550 | $2,550 |

| Deduct: Federal/provincial personal tax | ($746) | - | - |

| Deduct: Part I federal tax – refundable | - | ($782) | - |

| Deduct: Part I federal tax – non-refundable | - | ($204) | ($986) |

| Deduct: Provincial taxes – non-refundable | - | ($293) | ($293) |

| Equals after-tax investment income | $648 | $1,271 | $1,271 |

Sources: KPMG 2016 Personal Tax Rates, KPMG 2016 Corporate Tax Rates

The better part of a decade

After 10 years, the individual taxpayer (who has already paid taxes on the initial income, plus annual taxes on the 3% investment returns), has no additional taxes to fork over. Their portfolio is now worth $53,370.

Under the current corporate system, $8,368 of refundable taxes have accumulated, as well as $98,596 of active business income and after-tax investment earnings. The total taxable dividend amount of $106,965 ($8,368 + $98,596) is then distributed to shareholders and taxed in their hands as ineligible dividends – roughly 45.30% for an Ontario taxpayer in the top tax bracket. Once integration has supposedly done its job (so everyone ends up shouldering an equal tax burden), the business owner now has a net worth of $58,505. Whoops – that’s $5,135 more than the individual investor after 10 years ($58,505 vs. $53,370).

Enter the proposed corporate system, with its one tweak to eliminate refunds on all of a corporation’s passive investment income. Without the refundable taxes, that leaves only $98,596 (instead of $106,965) to distribute as taxable dividends to the shareholders. After they pay their personal taxes on the proceeds, they’re left with $53,928. That’s just $558 more than the individual investor ($53,928 vs. $53,370).

It would appear that the proposed system would come much closer to true integration between business owners’ and individual taxpayers’ investment interests.

After-tax portfolio value after 10 years (Ontario)

| Individual | Corporation: Current System | Corporation: Proposed System | |

|---|---|---|---|

| Portfolio value after 10 years | $53,370 | $98,596 | $98,596 |

| Add: Refundable taxes | - | $8,368 | - |

| Equals: Available dividends to distribute to shareholders | - | $106,965 | $98,596 |

| Deduct: Personal tax on dividends | - | ($48,460) | ($44,669) |

| Equals: Net worth | $53,370 | $58,505 | $53,928 |

Sources: KPMG 2016 Personal Tax Rates, KPMG 2016 Corporate Tax Rates

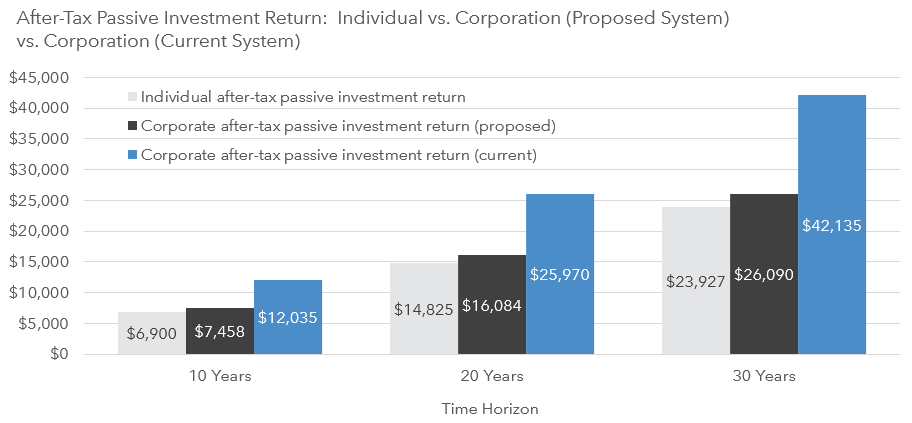

Every decade counts

As you might guess, under the current system, the further out we extend our illustration, the bigger the gap grows between individual and corporate after-tax passive investment returns. Below, I illustrate the dramatic difference the proposed change would make after 30 years.

Sources: KPMG 2016 Personal Tax Rates, KPMG 2016 Corporate Tax Rates

It ain’t over yet

As touched on above, everything I’ve just covered is still just a proposal, which means it is subject to change after the October 2, 2017 consultation period ends. That’s blog-job security for me, since I’ll want to take another look at it once the final results are in. Coming up next, we’ll see how capital gains are taxed within a corporation.

Great article! The end of refundable taxes might be controversial.

I study taxation in different countries, as well as low tax rates in different business areas. Thanks for the helpful article.

Justin, thanks for responding. Once again, it’s fundamentally unfair to compare a dollar earned by an employee to that in a private corporation. To equalize the level, you would have to account for all the benefits paid out to the employee. Largest one of them being pension. Taking also into consideration many years of education by some business owners and professionals, i.e. years of lost income / savings, one cannot argue that an employee should earn the same as the business owner. That’s not a fair comparison to start with. You make it seem that the proposed changes will make things more fair. This mentality by you and the government is deeply flawed. Instead of having a meritocracy where hard workers are making more, we’ll end up paying everyone the same. Soviet Union 2.0.

Thanks Justin. Won’t business owners just take these increased taxes and pass the bill onto the employee and customers? Less employee benefits/salaries and higher costs of goods/services for middle class consumers? They could even jack up prices even more than they are losing and claim it is the tax changes that caused this.

So is this really levelling the playing field or just making the gap between rich and poor larger?

@Dinesh: Great question – and I wish I had an answer. The truth is, no one knows what type of ripple effects the proposed changes will have. Passing the bill onto their employees and customers may not be a realistic outcome though (other competitors may keep the prices down).

There are a couple of issues you fail to mention

1. The entrepreneur is risking a lot to run the business. There has to be some kind of return to the years of zero income, debt accumulation, stress, and 14 hour days; whether you are a doctor (internship pays $7/Hour with 100 hour work weeks, and they spend 12-20 years training), a restauranteur (who starts off with one or two family employees and has a 30% chance of going bankrupt) or a manufacturer (who will be losing money for the first three years of business (on average). Compare that to a postal worker who starts earning right away.

2. The analysis completely ignores the fact that most employees at $100k have pensions. Compare a nurse and a doctor who are paid $100k/year. The doctor has no pension, no benefits, no overtime, no sick leave, no EI, no CPP.

3. It ignores the costs of the corporation.

4. The analysis really does not go into the issues regarding farmers, who are particularly hard hit with the inheritance/passing on of the family farm. These changes will destroy the family farm. It’s terrible.

5. Female entrepreneurs who have business expenses (say the owner of a massage practice) are particularly hard hit. The postal employee at $100k has maternity benefits and a guaranteed job when they return. Not so the entrepreneur. She will go on maternity. Office expenses are $33/square foot; if she has a typical 2000 square foot office, she will need almost $5,000 per month to run the office, plus her own mat costs. Retaining money in the corporation is essential to the business. Her business may not be there after she returns to work under the new rules.

@Tucker: I chose not to mention these counterarguments as they already overwhelm the content in countless articles since the proposals were released. In all honesty, I’m just bored of hearing the same message over and over again, and wanted to give my readers a fresh and unbiased perspective (and hopefully teach them a bit about corporate taxation in the process).

Does this take into account the other benefits salaried employees have in terms of paid vacation, health benefits and pension plans?

@Jim: This analysis does not take into account the other benefits or costs that salaried employees or business owners have.

Justin,

You miss the point in that small business owners use corporations for everything, not just to buy equipment, but for mat leave, pension, sick leave, vacations, etc. A dollar in the corporation is not a dollar paid to an employee, as technically, you pay employee more in benefits. How much does a small business owner have to save in the corporation to retire at 65 with a “defined benefit pension” of 65K till 95? That’s all done within the corp. What about the risk a business owner takes? Is the society right to pay a 9-5-er the same as a business owner who has no defined work hours?

So you need to be honest about those things before depicting the pure taxation impact.

@Artur: Being a salaried employee has its perks, but it also has its downsides. Being a business owner has its perks, but it also has its downsides.

Great article Justin,

It clearly paints a picture of why this is being done. Nobody wants to pay more taxes, but sometimes someone has to.

@Rob: Thanks!

Justin,

your post/blog is by FAR the most clear explanation on the subject out there. Agreed specifically for dividends, but what about capital gain or interest income? Keep ’em coming, its a pleasure to read you.

@Pete: Thank you for your feedback! My most recent posts have already focused on the taxation of passive interest income in a corporation (so I think I’ve beaten that topic to death) – please feel free to check them out if you haven’t already. The next three corporate taxation blogs are already in the works, and will deal with capital gains:

– Taxation of Capital Gains in a Corporation

– Tax Gain Harvesting in a Corporation

– The End of the Capital Dividend Account?

Thanks for the clear depictions. Very nice to see someone actually explaining the changes and effects on using a corporate structure for investment savings.

@Phil: You’re very welcome. I’ve found that most of the news articles circulating around sound exactly the same, and don’t add anything to the discussion (I’m a big fan of using examples to paint a clearer picture for my readers).

Justin,

Are you not making the assumption that the corporation is solely utilized as a tax shelter? For those businesses that need to accumulate or maintain capital reserves as a part of their core business (i.e. everyone from contractors to developers to restaurants and dental practices and auto body shops). For most businesses that are actual operating businesses, as long as that capital – along with any investment income it may have earned – remains in the business, it is capital that is completely at risk for the business owner. In your example for example, if something happened to the business in year 9, that $98,596 portfolio could disappear in a puff of smoke even though it was – for the company – after tax dollars. You also don’t take in to account that the personal investment portfolio could will take place within an RRSP that would provide the individual taxpayer with sheltered/tax deferred income not available to the company in addition to creating a tax refund that could also be reinvested. While your math and your spreadsheet is undoubtedly correct I believe you are in error for not making any allowance for risk. I think you would be more correct in identifying the current systems $5,135 potentially higher value after a 10 year investment horizon as a pretty nominal 5.36% risk premium.

@Ken Cantor: If a small business owner was using the corporation to accumulate funds for their future business needs, they would still only initially be taxed 15% on their business income. They would then have much more capital to deploy to build their business (which is what the government would like them to do). If they earn some interest on these savings in the meantime, the proposals are not going to penalize them relative to an individual investor (it’s just not going to give them a tax advantage for investing in a passive investment portfolio within their corporation).

Business owners also have the ability to pay out a salary and contribute to an RRSP account. The Ontario taxpayer in this example is already in the highest tax bracket, so they would presumably have maxed out their RRSP account already (so my comparison of a business owner investing within a non-registered corporate account vs. a high income salaried employee saving their after-tax income in a personal non-registered account seems to me to be a fair comparison).

I’m not clear how your example of the business owner who loses everything relates to this example. If they were to lose $98,596, they wouldn’t be able to obtain the refundable taxes anyway, as they would have no available dividends to distribute to themselves. So if you run your business into the ground, the new proposals shouldn’t impact you. And if your business is successful, then taking more risk paid off for you (even without an additional tax advantage).

Great answer.

It’s clear that not everybody (including me) exactly what these changes are meant to do.

Great post, and thanks for leaving the politics and indignation out of it. As a business owner who has an op-co/hold-co structure, these changes will directly impact me. But taking a dispassionate look at things, it seems pretty obvious that the passive income changes are needed in the interest of fairness, as is the income sprinkling. I have no children, but my brother who is my business partner does (as does a cousin in a near identical setup). Why should they get to pay a lower tax rate than I simply because they had children? Andrew Coyne @ National Post has had a couple excellent columns on this as well.

I won’t pretend to understand the third change relating to capital gains. I don’t believe my accountant has ever recommended any aggressive tax planning using that method.

@Marcel: Thanks – I’m not really one for politics :) The change relating to capital gains is relatively aggressive, so it’s probably better that your accountant never recommended it.

Nice article Justin. It appears to me that if the incremental costs of starting and maintaining a corporation were taken into account, that any advantages of incorporating could easily disappear. Maybe the real losers if this change comes to pass, will be the lawyers and accountants… Costs matter.

@Garth: Thanks, Garth! You forgot another real loser of these proposed changes…the portfolio managers! :)

What are the numbers if the tax bracket is lower, say 50,000 in AB

@R Butgereit: I’m not sure – but feel free to adapt your own figures using the downloadable excel spreadsheet I’ve included above.

Thanks Justin,

As usual, you’ve presented the info in an easy to understand, seemingly unbiased, format.

Based on your article, it seems the government might actually be getting this right.

Joe

@Joe: I was quite surprised at how easily integration was improved by making all the corporate taxes non-refundable. There are other complexities to this approach that the government is still trying to simplify if possible (which is why they’ve provided the consultation period).

Thank you Justin for this post!

Just 2 comments:

1) This does not take into account that there is a real accounting and legal cost to maintain a corporation. The benefit can be quite moot, even under the current rules, if the amount for passive investing is low or if the timeframe is small for deferral.

Say it costs me 3500$ per year to maintain the corp; compounding this amount at 3% after 30 years this costs me 180000$! This could wipe out any advantage if amount invested is low or timeframe for deferral is small.,

2) To legally circumvent the proposed changes, do you think flowing the money through a TRUST would help?

Thanks

D

@D: I completely agree that the accounting and legal costs of maintaining a corporation can offset any benefit of tax deferral in the current system if the business owner is not saving enough within the corporate investment account.

I can’t immediately think of a way that a trust could be used to legally circumvent the proposed corporate changes.