In Episode 10 of the Canadian Portfolio Manager Podcast, Justin analyzes the historical returns of gold from 1972 to 2019 to help Canadian investors decide whether the shiny yellow metal deserves a place in their portfolio. Using the data, Justin sets out to determine if any of the hype is warranted – has gold historically been a decent safe haven, portfolio diversifier, return enhancer and/or inflation hedge for Canadian investors? At the end of the show, we pit two gold ETFs (IAU and GLD) against one another in our ETF Kombat. And for all you visual learners out there, the “Investing in Gold” video, “ETF Kombat: IAU vs. GLD” video, and podcast script are also available below.

- Ask Bender: Kevin from Edmonton asks whether he should include a 5% strategic allocation to gold in his portfolio [0:00:46.10]

- John Bogle discusses why gold is a speculation, not an investment [0:01:19.10]

- Was gold a safe haven for investors during the financial crisis and the global pandemic? [0:04:54.10]

- Correlations between gold and stocks/bonds between 1972 and 2019 [0:07:29.10]

- Why Kevin O’Leary likes gold [0:08:13.10]

- Has gold historically reduced the risk of a balanced portfolio? [0:09:02.10]

- Why Ray Dalio believes investors should hold 5-10% of their assets in gold [0:10:38.10]

- Has gold historically been a return enhancer (i.e. provided higher risk-adjusted returns for investors)? [0:11:55.10]

- Has gold historically been positively correlated with Canadian inflation? [0:13:24.10]

- Asset class performance between 1972 to 1979 (when Canadian inflation averaged 8.7%) [0:14:22.10]

- Would a balanced portfolio have kept up with inflation between 1972 and 1979? [0:15:19.10]

- Gold as an inflation hedge between 1980 and 2019 [0:16:18.10]

- Insights Canadian investors can take away from this analysis [0:17:19.10]

- If you decide to add a bit of gold to your portfolio, Kevin O’Leary has some practical advice for you [0:19:13.10]

- ETF Kombat: IAU vs. GLD (gold ETFs) [0:20:52.10]

Podcast 10: All That Glitters Are Gold ETFs (Script)

Welcome to episode 10 of the Canadian Portfolio Manager podcast, where we help you become a better ETF investor. I’m your host Justin Bender, and in today’s show we’ll be discussing that shiny yellow metal many investors can’t get enough of these days. Recently, there seems to be more love than usual for this precious metal, and it’s easy to see why. As of September 30th, 2020, gold prices were up around 27% year-to-date in Canadian dollar terms, while Canadian stocks (even including dividends) hadn’t quite broken even yet.

You may now be wondering if you should be adding gold to your portfolio, and you’re certainly not alone. I’ve been busy fielding many investor questions, like this recent one:

Kevin from Edmonton: Hi Justin – it’s Kevin from Edmonton here. I’ve been considering adding a 5% strategic allocation to gold in my portfolio. Does this make sense from the risk and return perspective of a Canadian investor, or am I just complicating my portfolio? Thank you!

In the past, I’ve never recommended gold to my clients, for many of the same reasons the late, great Vanguard Group founder John Bogle – or “Jack” to his friends – explained in this 2011 CNN Business interview:

John Bogle: Gold is not an investment, at all. Gold, is a speculation. It has absolutely no underlying intrinsic value. Bonds are ultimately supported by interest coupons. Stocks are supported by dividend yields and earnings growth. And gold is supported by, well, the ability to think somebody else is going to take it off your hands for more than you paid for it. It doesn’t have an internal rate of return, so it’s a speculation. Is it a good speculation today? I don’t know if I would be much of an expert on that … but it’s gone so high, so far, that I’d be very skeptical of it. But if you really are bitten by the gold bug (and it seems like an awful lot of people have been bitten by the gold bug), and if you want to speculate, maybe 1 or 2 or 3 or 5% of your assets in gold is not the worst idea in the world, but I wouldn’t do it myself, and I wouldn’t advise most investors to do it.

Some of you may not know this, but Bogle’s book, Common Sense on Mutual Funds, was the gateway drug that eased my journey into the passive investing world. I admired Bogle’s investor advocacy. Without him, I may never have created the Canadian Portfolio Manager blog, YouTube Channel, or even this podcast that you’re listening to now.

So, suffice it to say, whenever Jack spoke, I listened.

That’s why I was thrown off when Bogle announced in a 2018 MIT Laboratory of Financial Engineering interview that he had been hiding a dirty little secret in a scholarship fund he was managing at the time:

John Bogle: I hope you’re sitting down … 5% in gold.

Bogle went on to explain he had included a 5% gold allocation in the fund to hedge against the risk of “some kind of catastrophe”. This got me thinking – if legendary investor John Bogle could come around to the idea of holding some gold in a portfolio, perhaps I was missing something.

Another advocate for holding gold in a portfolio is billionaire Ray Dalio, founder of Bridgewater Associates. As the world’s biggest hedge fund firm, Bridgewater managers around $138 billion US. In an August 2019 LinkedIn post, Dalio wrote:

“If you don’t have 5-10% of your assets in gold as a hedge, we’d suggest that you relook at this. Don’t let traditional biases, rather than an excellent analysis, stand in the way of you doing this.”

So that’s precisely what we’re going to set out to do today. To prepare for this episode, I combed through all the data I could lay my hands on. What I learned was this: Someone with lots of data but little integrity could easily sway an investor to be for or against gold, depending on which particular periods they showcased.

In other words, it’s all too common for financial gurus to cherry-pick investment periods to make their desired point. For example, gold’s prospects can brighten or dim considerably depending on whether or not the analysis includes its shiny returns from the 1970s.

I’m not going to use the information I’ve gathered to persuade you in either direction. I’ll simply provide you with the data and its context, to help you make a more informed decision. And as this is a Canadian investing podcast, all data will be provided from a Canadian perspective.

So, welcome to today’s safe haven for tackling the arguments for and against investing in gold. Is gold itself a safe haven, portfolio diversifier, return enhancer, and/or inflation hedge? You get to decide.

Gold as a Safe Haven

Let’s begin with whether gold might be a good safe haven during turbulent times. As Warren Buffett explained in a 2011 CNBC interview:

“Gold is a way of going long on fear, and it’s been a pretty good way of going long on fear from time to time. But you really have to hope people become more afraid in a year or two years than they are now. And if they become more afraid you make money, if they become less afraid you lose money.”

Although Buffett is famously known for favoring a Cherry Coke over bars of bullion, he acknowledges it’s something investors flock to when their instinctive fears kick in, pushing up its price. Others oppose investing in gold by pointing to the global financial crisis. They claim gold prices barely budged during this extreme event.

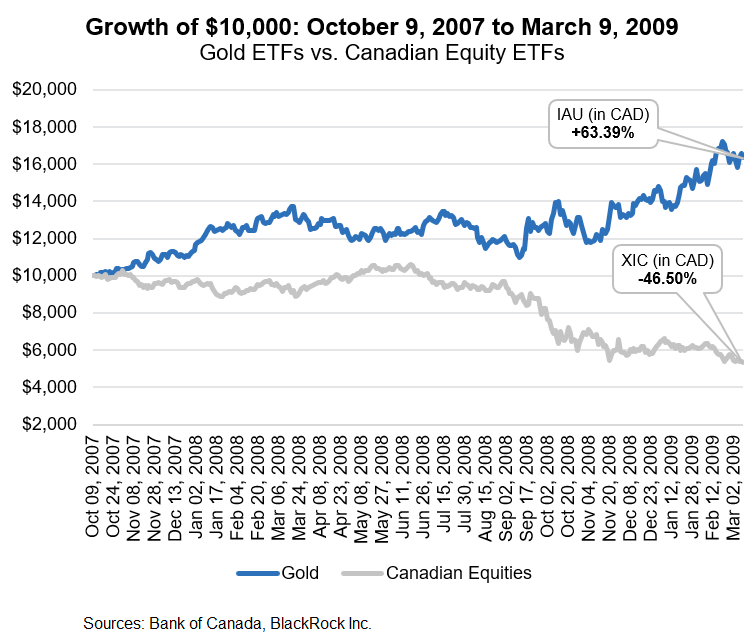

So, who is right? I’ll award this round to the gold bugs by focusing in on the worst 17 months of the global financial crisis, from October 9th, 2007 to March 9th, 2009. During this period, Canadian equity ETFs lost around 46% of their value. U.S. and international equity ETFs lost around 42% and 49% respectively, in Canadian dollar terms. But over the same period, gold ETFs increased in value by a whopping 63% in Canadian dollar terms.

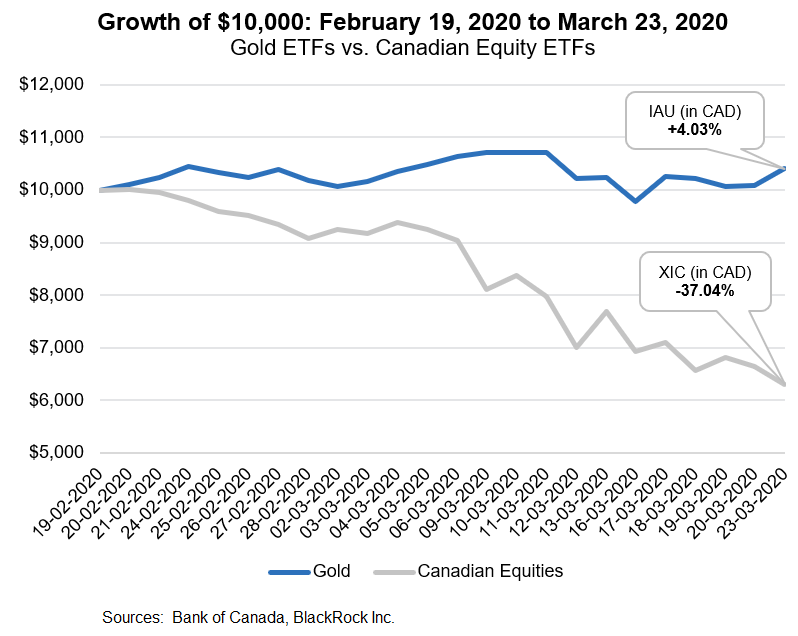

And what about during the global pandemic of 2020? Well, during the worst 33 days so far, Canadian equity ETFs lost around 37% of their value. Gold ETFs held steady during this uncertain time, increasing by 4% in Canadian dollar terms.

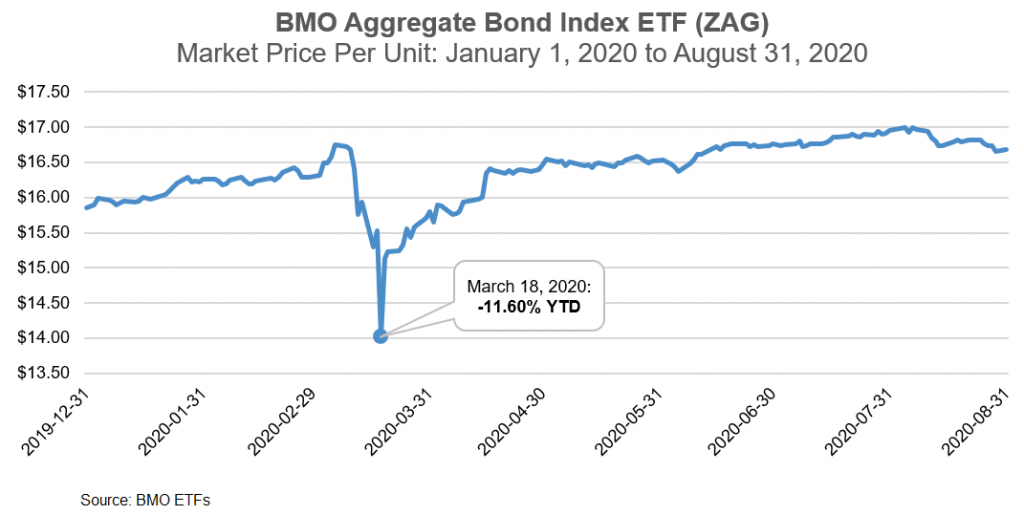

Although a 4% price gain may not sound too impressive, compare that to the instability of supposedly “safer” bond holdings during this volatile period.

It was difficult, if not impossible, to rebalance a portfolio by selling bonds and purchasing equities, without taking a steep haircut on the bond prices. Liquidity in the fixed income markets had basically dried up.

In contrast, if you’d had a 5% allocation to the more stable-priced gold ETFs, it would have been a snap to sell them and rebalance into equity ETFs with the proceeds. Although a 5% cash allocation would also have provided this same liquidity benefit, gold could have served as a back-up plan.

Gold as a Portfolio Diversifier

Gold advocates also often suggest that adding a lump of it to your portfolio offers a smoother investment ride. They claim, because gold has historically been uncorrelated to equities and fixed income, it can reduce the portfolio’s overall volatility or risk.

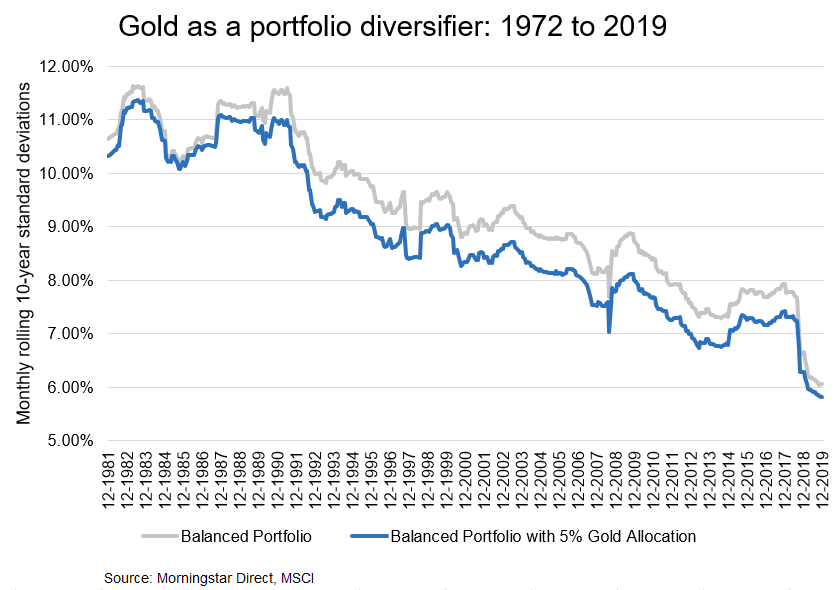

Looking at the data between 1972 and 2019, gold prices do appear to be uncorrelated with the returns of these traditional asset classes. During this timeframe, gold had a correlation of 0.01 to global equities, 0.06 to Canadian equities, and 0.03 to long-term Canadian bonds. These numbers indicate a very weak or non-existent relationship between gold and these other investments.

But don’t take my word for it. Kevin O’Leary, Canadian businessman and star of the reality tv series Dragon’s Den, holds a bit of gold for its portfolio-stabilizing properties. In a 2011 interview for Kitco News, O’Leary discusses why he likes gold:

Kevin O’Leary: I like gold because, in a way, it’s a stabilizer, it’s an insurance policy. You know, I listen to all the gold pundits, and they’re always wrong, as far as I’m concerned. It’s impossible to time the moves. I’ve owned gold for decades, and I simply have a 5% weighting. I look at it quarterly. When it becomes more than 5%, I sell into the strength, and when it weakens, I buy into the weakness. It’s just a stabilizer. You know, I’m not one of those guys that’s going to go to a 40% weighting in gold. I don’t believe the hyperinflation story, it hasn’t happened. Gold is popular for a whole host of reasons. And 5% seems to be enough. It’s worked for me in portfolio management. It’s the only security I own that doesn’t pay a dividend.

So is “Mr. Wonderful” onto something with his claims of gold as a portfolio stabilizer? Turns out, the gold bugs are right again. (ding ding sound)

To demonstrate, we’ll compare two balanced portfolios from 1972 through 2019. Our first portfolio – we’ll call it our “shiny” portfolio – has a 5% weighting to gold. Our “plain” portfolio has no gold.

I began the analysis in 1972 because that was the first full calendar year after the U.S. abandoned the gold standard in August 1971. For both portfolios, I rebalanced them annually; split the equity allocations 30/70 between Canadian and global stocks; and used long-term Canadian bonds for the fixed income portion, as these returns were available prior to 1980.

The plain portfolio’s allocation is 60/40 stocks and bonds. The shiny portfolio carves its gold out of the 60% stock allocation … so its allocates 55% to stocks, 40% to bonds and 5% to gold.

What were the results over the 48-year analysis? The shiny portfolio had a lower standard deviation of 8.7%, compared to the plain portfolio’s higher standard deviation of 9.2%.

So, adding a 5% gold allocation to a balanced portfolio reduced the risk between 1972 and 2019. In fact, in 100% of the rolling 10-year periods during this timeframe, the shiny portfolio would have been less volatile than our plain one.

It seems clear that adding a bit of gold to a portfolio has historically smoothed the ride for investors, which could be a good behavioural argument for including gold in your portfolio.

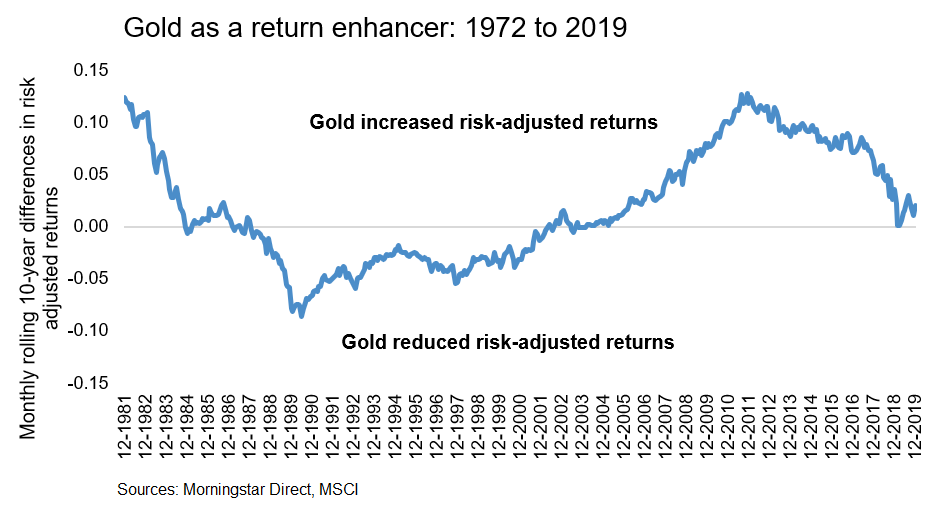

Gold as a Return Enhancer

Now, lower volatility is great, but higher risk-adjusted returns are even better. In a 2019 LinkedIn post, Ray Dalio wrote that he too believes gold is an effective portfolio diversifier. But he goes even further, suggesting it can reduce risks and enhance returns. As mentioned earlier, Dalio feels all investors should allocate between 5% and 10% of their portfolio to gold.

Ray Dalio: I think every portfolio should have the right amount of diversification in it. I believe it (gold) always should be a certain part of a portfolio, because there’s a certain environment that it diversifies the portfolio well, and a certain environment to worry about.

On the other hand, investors like Warren Buffett would argue that gold is an unproductive asset, so including it in a portfolio will likely hurt your portfolio’s returns over time.

Warren Buffett: A productive asset of any kind, a decent productive asset is going to kill a non-productive asset over time. Now, in any given 1-year period, 5-year period, any asset can outperform another asset.

Warren Buffett: I will guarantee you that farmland (over a hundred years) is going to beat gold, and so are equities.

Well, I doubt any of us will be around in a hundred years to collect on Buffett’s guarantee, so let’s look at the data we have to determine who is right.

From 1972 to 2019, a balanced portfolio with a 5% gold allocation returned 10.2% on average, while a balanced portfolio without gold also returned 10.2%. This suggests the portfolio’s overall return was not impacted either way. But as we just discussed, the balanced “shiny” gold portfolio had a lower standard deviation of 8.7%, vs. 9.2% for the “plain” portfolio. This results in a slightly higher risk-adjusted return for the gold portfolio: 0.49 vs. 0.46.

Now, this 48-year period is likely longer than many investors’ time horizons. So, let’s just look at 10-year rolling time periods. What if we use the Sharpe ratios for each portfolio to plot the difference between their monthly rolling 10-year risk-adjusted returns? Doing so, we find the shiny portfolio had higher risk-adjusted returns than the plain portfolio around 58% of the time, leaving around 42% of rolling 10-year periods where it underperformed. During the 1970s and 2000s, adding gold to a portfolio contributed favourably to its risk-adjusted returns. It detracted from them during the 1980s and 1990s. As Dalio reasons, there will be periods, like the 1970s and 2000s, when gold diversifies the portfolio well, and other periods, like the 1980s and 90s, when gold is a drag.

Gold as an Inflation Hedge

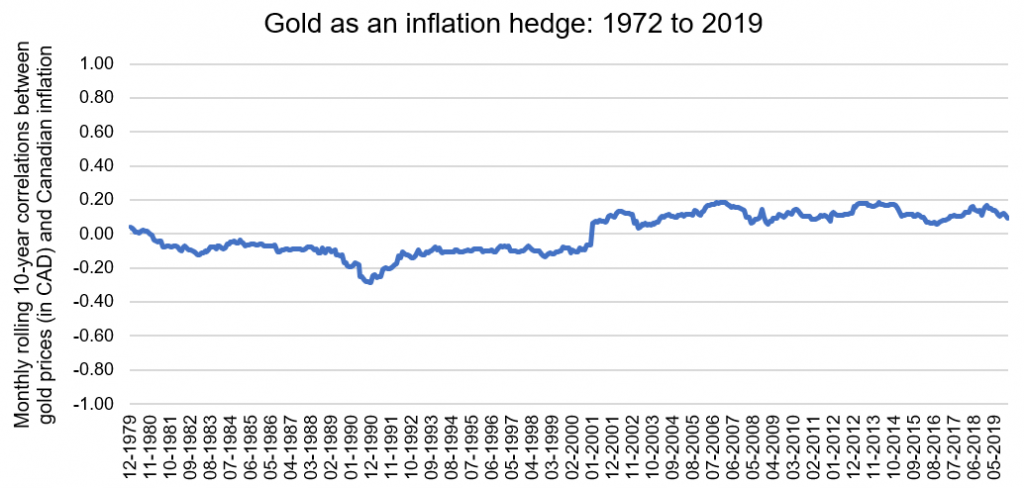

Last up, we’ll tackle the concept of gold as an inflation hedge. Many gold advocates point to the 1970s as proof of its purchasing power protection. However, between 1972 and 1979, Canadian inflation and gold prices (in CAD) had zero correlation. Over our entire measurement period, the correlation was only slightly higher, at positive 0.04, indicating little to no correlation between Canadian inflation and gold prices.

Even over monthly rolling 10-year periods during our entire measurement period, we see nothing that indicates gold has much correlation to Canadian inflation. During the worst 10-year inflationary period between 1973 and 1982 (when annual inflation in Canada averaged 9.7%) the correlation between Canadian inflation and gold prices was a somewhat surprising negative 0.11.

Source: Morningstar Direct

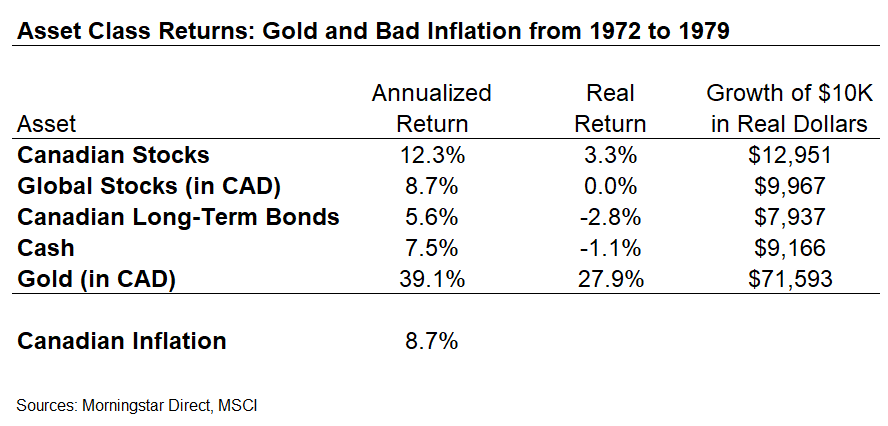

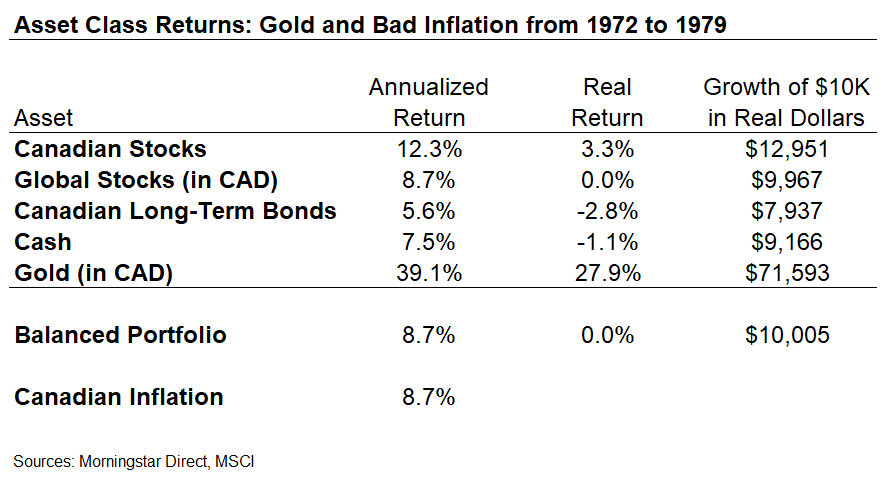

In 2012, U.S. authors Craig Rowland and J.M. Lawson published a book called “The Permanent Portfolio.” In it, they provided U.S.-based pre- and post-inflation returns between 1972 and 1979 for a number of asset classes … including gold. Over the entire period, all asset classes had positive gross returns. But once they adjusted for an average 8.1% annual inflation, only gold provided positive real returns.

From a Canadian perspective, inflation averaged slightly higher – around 8.7% over the same period. Canadian and global stocks (in Canadian dollar terms) did better, with real returns of 3.3% and 0% respectively. Unfortunately, long-term Canadian bonds and cash didn’t fare as well as stocks, with real returns of -2.8% and -1.1% respectively.

So sure, it would have been nice to have a little gold in your portfolio during the 1970s. It had a real return of nearly 28% per year in Canadian dollars. But it wasn’t absolutely necessary to include gold in your portfolio to keep up with inflation.

A Canadian investor could have held their own by investing in traditional asset classes instead. For example, consider a simple balanced portfolio, with 5% in cash, 35% in Canadian long-term bonds, 18% in Canadian stocks and 42% in global stocks. The portfolio would have earned an annualized return of 8.7%, during a period when inflation also averaged 8.7%, netting a real return of 0% during this period of supposed inflation Armageddon.

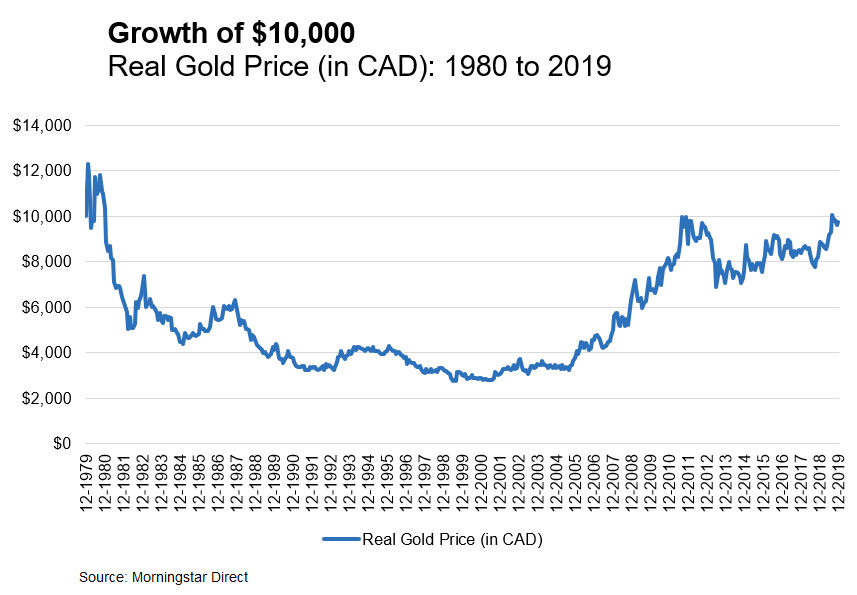

Over the next 40 years, from 1980 through 2019, the price of gold did manage to keep pace with Canadian inflation. Inflation averaged around 3% during this period, with a similar average return for gold in Canadian dollar terms.

Then again, as a stable store of value, gold was anything but. Between 1980 and 1999, gold lost nearly 70% of its value in real terms.

Take a moment to let that sink in. If you had invested $10,000 in gold in 1980, your investment would have lost nearly 70% of its real value over the next 20 years, so it would have been worth around $3,000 in real terms at the end of 1999.

Over the following two decades between 2000 and 2019, gold enjoyed some recovery, but its real price only occasionally reached its original $10,000 value.

Thirty to forty years seems like an extremely long time to wait for an asset class to recover just enough to maintain its purchasing power. I can’t imagine many investors with the patience to continue rebalancing this torturous portfolio across multiple decades … just to basically break even.

So now that we know the historical data for gold from a Canadian perspective, what insights can Canadian investors take away from it all?

- First, even Warren Buffett seems to agree that gold is likely a decent safe haven for investors. If you’re someone who panics during market downturns, perhaps having a slice of gold in your portfolio could keep you from making more impulsive decisions. But while you’re asking yourself this, also ask yourself if you have the right mix between stocks and bonds. Increasing your fixed income allocation could be a more suitable alternative for calming your nerves during troubled times.

- Second, gold has historically diversified a traditional stock/bond asset mix, offering lower portfolio volatility. Once again, if you’re a nervous investor, this may help you stay invested during the many market downturns we have yet to experience. But again, ask yourself whether you should consider holding more fixed income instead of gold.

- Third, it appears gold has historically been a return enhancer more often than not. It seems to work especially well when investors need it the most. This attribute could warrant including a small allocation to gold in your portfolio.

- Fourth, if you’re looking for an effective hedge against inflation, you should probably keep looking. Although holding gold may fit the bill over extremely long investment horizons, there doesn’t appear to be much evidence it’s a decent inflation hedge over shorter timeframes, which are more relevant for the average investor.

- Fifth and most importantly, gold may have its benefits if you don’t go crazy over it. But if it’s going to distract you from your greater priorities – that is, being a patient, low-cost, index investor – you may be better off ignoring its allure. And besides, wouldn’t you rather invest in a single asset allocation ETF instead, leaving you with more time to spend with your loved ones?

The Simpsons: Honestly, no, I’d rather have the gold.

All of this begs a question: Even if you would like to add some gold to your portfolio, it’s currently hovering around record highs. Have you already missed the boat?

If you go ahead and buy in at this time, you’d best be comfortable with the very real possibility its price might decrease significantly after you do. The price could also stay deflated for many years, testing your patience as a disciplined investor. Keep this in mind as a critical factor as you consider your next steps.

In his 2011 Kitco interview, Kevin O’Leary also cautioned investors against buying gold when everyone else is buying it:

Kevin O’Leary: When everybody is saying you gotta own it, you should be selling it. Because when it corrects, it doesn’t touch the sides on the way down. So I simply say 5% is good for me. Some people like it 10, 15% weighting, I’m a 5% guy. And I’m disciplined about it. I hope it runs to $5,000, I don’t care. I’ll be selling selling selling selling all the way up, keeping it at 5%, and when it corrects back down to $2,000, I’ll be buying it in. It’s fun! That’s the way you should work with gold, never get so caught up that you take all your dividend yielding securities, that are also a hedge against inflation, and put it into a commodity like gold.

Whether you decide on a 1, 2, 3, or 5% allocation to gold, I suggest taking O’Leary’s advice and remaining disciplined. Have a strict rebalancing schedule in place to adhere to, no matter what. If gold prices decline, you can buy more to bring your portfolio back on target. If they increase, you can sell some shares of your gold ETF to keep it from overtaking the interest and dividend-yielding securities in your portfolio.

We’re almost done, with one more housekeeping conversation to cover. If you decide to include a small allocation to gold in your portfolio, how will you get it done? Trust me, gold bars weigh a ton, so you’ll want to invest in a reasonably priced ETF to gain the desired exposure.

Which one? This brings us to our final segment of today’s show:

ETF KOMBAT!

Let’s take on all that glitters by pitting two gold ETFs against one another.

In one corner, weighing in at over 1,200 tonnes, we have our heavyweight champion, the SPDR® Gold Trust, with ticker symbol GLD. And in the other corner, weighing in at around 500 tonnes, you’ll find our middle-weight contender, the iShares Gold Trust, with ticker symbol IAU.

Which will achieve total dominance over your investment dollars? Although both funds transact in U.S. dollars and provide investors with exposure to the returns of gold, this match will determine which of them is worth their weight in it.

Round 1

FIGHT!

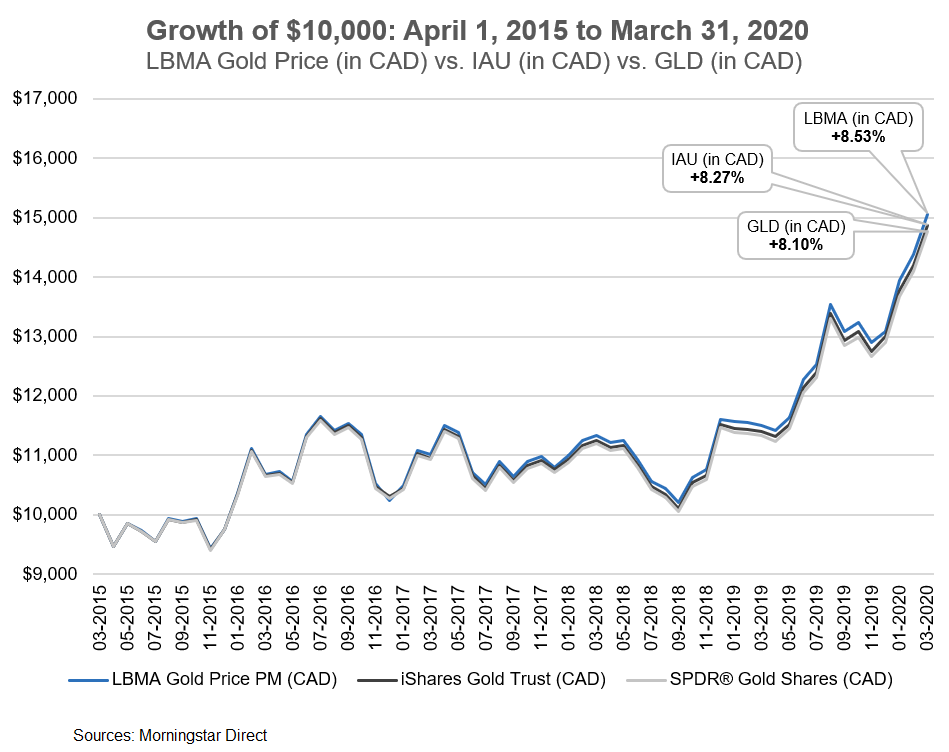

Since the end of March 2015, IAU and GLD both began tracking the LBMA (or London Bullion Market Association) Gold Price. Over the next 5 years ending March 31st, 2020, this reference benchmark returned 8.53% on average in Canadian dollar terms. Over the same period, IAU and GLD returned 8.27% and 8.10% respectively (in Canadian dollar terms).

The difference between the funds’ returns and the return of the LBMA Gold Price reference benchmark was mainly the result of each fund’s product fees. IAU has an annual sponsor fee of 0.25%, lagging its benchmark by an average of 0.26% each year. GLD has a gross expense ratio of 0.40%, lagging the same benchmark by 0.43% annually.

5-Year Annualized Returns (in CAD): March 31, 2015 to March 31, 2020

| Security | Gold ETF Return | LMBA Return | Difference | Product Fees |

|---|---|---|---|---|

| iShares Gold Trust (IAU) | 8.27% | 8.53% | (0.26%) | (0.25%) |

| SPDR® Gold Trust (GLD) | 8.10% | 8.53% | (0.43%) | (0.40%) |

Remember, in investing, you rarely get more by paying more. Weighed down by bloated product fees, our top-heavy contender couldn’t compete with its trimmed-down counterpart when it comes to end returns.

IAU wins.

Round 2

FIGHT!

What’s an ETF unit price among friends? If you’re a long-term, buy-and-hold investor, IAU’s and GLD’s differing share prices shouldn’t matter much. Then again, all else equal, lower share prices can end up costing you when trading ETFs. That’s because you end up paying a higher bid-ask spread, which is the difference between what an ETF share costs you, versus what you can sell it for. It’s simple math: If you’ve got more shares to unload, you’ll incur more bid-ask spread costs than if you’re only selling a few.

Let’s take an example of two investors, Wayne and Garth, who both invest $100,000 U.S. in a gold ETF. Wayne decides to purchase 542 shares of GLD, at an ask price of $184.50 U.S. Garth decides to purchase 5,420 shares of IAU at an ask price of $18.45.

Immediately after purchasing their shares, Wayne and Garth realize they just bought a hunk of metal that doesn’t do anything. They both sell all their GLD and IAU shares at their current bid prices of $184.49 and $18.44 respectively.

| Symbol | Ask Price (A) | Bid Price (B) | Shares (C) | Proceeds of Sale (B × C) |

|---|---|---|---|---|

| GLD | $184.50 | $184.49 | 542 | $99,994 |

| IAU | $18.45 | $18.44 | 5,420 | $99,945 |

| Difference | $49 |

That’s just a penny’s spread for both … but those pennies can add up! Compared to Garth, Wayne ends up with an additional $49 U.S. from the sale proceeds. This was due to the higher share price of GLD, relative to IAU (which assumed the same bid-ask spread cost per share of a cent). Even if GLD had a much wider bid-ask spread of, say, 5 cents instead of a penny, it would still have had higher sale proceeds than IAU.

| Symbol | Ask Price (A) | Bid Price (B) | Shares (C) | Proceeds of Sale (B × C) |

|---|---|---|---|---|

| GLD | $184.50 | $184.45 | 542 | $99,972 |

| IAU | $18.45 | $18.44 | 5,420 | $99,945 |

| Difference | $27 |

Again, for buy-and-hold gold ETF investors, IAU’s lower cost would be expected to outweigh GLD’s slightly reduced trading costs. But if you’re planning to be a hyperactive gold trader (which I wouldn’t recommend in general), you’ll give away a little less with each GLD trade.

GLD wins.

That’s gold, Jerry. GOLD!

Round 3

FIGHT!

Most Canadian investors prefer to transact in Canadian dollars. Unfortunately, both IAU and GLD trade in U.S. dollars. This makes portfolio rebalancing more difficult and costly, since you will need to periodically buy or sell your U.S.-based gold ETF shares when rebalancing a portfolio that includes Canadian-based ETFs. To do so, you’ll EITHER need to:

- Convert your U.S. dollars to loonies (or vice versa) at your brokerage’s relatively high currency conversion rates … OR

- Sidestep the steep FX conversion costs by using the Norbert’s gambit strategy.

Luckily, BlackRock provides a Canadian-dollar version of IAU, called the iShares Gold Bullion ETF (with ticker symbol CGL.C). Although CGL.C has a higher MER (or management expense ratio) of 0.55%, investors could consider holding up to half their gold allocation in IAU, and the other half in CGL.C for rebalancing purposes. The weighted-average product costs for this combination would be 0.40%, which is the same expense ratio as GLD.

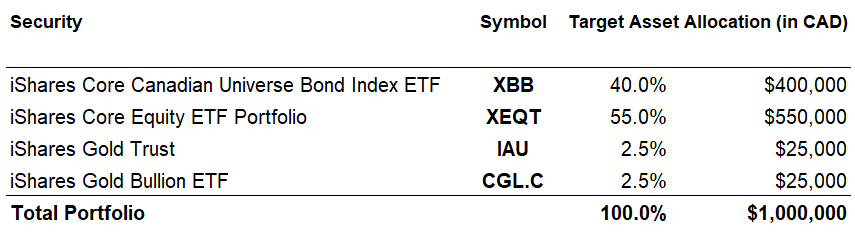

As an example, suppose you invest 40% of your $1,000,000 portfolio in a Canadian bond ETF, like XBB, 55% in an all-equity ETF, like XEQT, and 5% in gold ETFs, split evenly between the U.S.-based IAU and Canadian-based CGL.C.

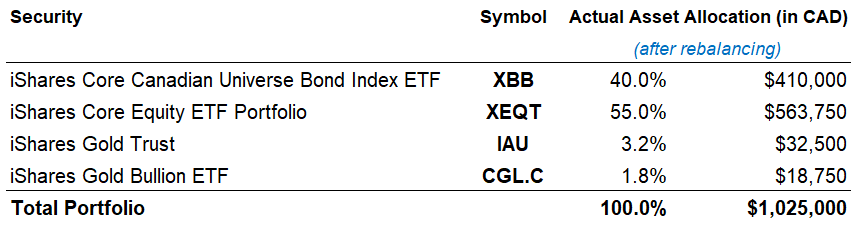

After a few months, your bonds increase in value by 2.5%, your stocks don’t budge, and your gold ETFs increase by 30%.

If you wanted to rebalance back to your original targets, you could sell around $13,750 of CGL.C, which would settle in Canadian dollars. You could then buy $13,750 of your all-equity ETF, XEQT (which also transacts in Canadian dollars), bringing your portfolio back in balance.

FINISH IT!

At no point during this portfolio rebalance were you required to convert between U.S. and Canadian dollars. By holding a combination of IAU and CGL.C for your gold allocation, you can reduce the brokerage costs associated with currency conversions when rebalancing, while still keeping your overall product fees in line with GLD.

IAU wins.

METALLURGY!

That’s it for today’s golden episode – thank you again for taking the time to tune in. As you probably gathered, I’m still lukewarm about the idea of including gold in a portfolio. It just seems like an unnecessary complication with only a modest amount of potential benefit. But if you need to scratch that itch, perhaps consider including a small allocation for now – maybe 2-3%. If gold prices plummet, you can decide then whether you want to boost your target allocation up to 5%.

Also, if you’re using a one-ticket asset allocation ETF, I wouldn’t even bother adding any gold. You’ll just over-complicate a portfolio that was meant to keep things simple. Maybe buy yourself or your sweetie a nice little piece of gold jewelry instead.

Until next time, stay safe and stay the course!

I have been using a 5% position in Gold producers (XGD) as my gold hedge for about the last five years. While I certainly have not performed the extensive testing you have, over the period I have owned it, it has performed very counter cyclically to my other equity positions (EQL,XUU and XEI). Additionally as they (XGD) are active businesses albeit in the gold/precious metals business, it seems to me that they address Buffett’s concerns about gold being a non producing asset and currently it is yielding about 2% .

I note that you don’t comment on after-tax returns for ETFs vs physical gold, which i undferstand is capital gains-free. I have about 10% of my equity in Maple Leafs, and have been sitting on them for over 20 years, even before ETFs were a thing.

I’m a bit late on this post, but since I just re-listened to the podcast (as I once again tackle the gold question), I wanted to say thanks for another great podcast (and I laughed out loud at the perfectly placed Simpsons sound-bite)!

I know gold has generally been shunned by the indexing supporters (Bogle and Buffett most notably) and I’ve always bought their arguments, but the pandemic crash has made me rethink things a bit: the idea of bond prices rising due to interest rate cuts seemed to initially be outweighed by investors worried about default risk (I assume mostly on the corporate side), and as you mentioned, bonds became illequid (I guess you could still sell a bond ETF, but you’d take a pretty decent haircut).

Yet, as you mentioned, I can’t really bring myself to purchase gold at near-historic highs, given some of decade long sluggish returns. I’m thinking maybe a better alternative would be to hold 5% in short-term US treasuries on the theory that in an emergency investors tend to flee to to US dollars, and specifically t-bills (VGSH prices in early 2020 seemed to prove this out). It would be similar to holding cash, but likely better stabilization effects in a crash. I’d personally be comfortable taking this 5% from my fixed income, but understand others may disagree due to the currency risks.

I’m curious if you’ve considered anything similar or if the early pandemic bond illiquidity has made you rethink fixed income allocation at all?

@Graeme – I’m glad you found the gold podcast entertaining :)

I haven’t considered holding a small USD cash allocation, but I don’t see anything wrong with the concept (I would probably opt to just hold a 5% CAD cash allocation instead though, as there is already sufficient USD exposure in the U.S. equity ETFs). After witnessing the bond illiquidity during the pandemic, it did make me appreciate the benefits of holding some liquid cash in a portfolio.

Sorry this is a little off topic but I thought I’d post here since this is the latest blog post.

Do you have any plans to perhaps make an investment tracking spreadsheet on Google Sheets? You put together such an amazing tool for us but I don’t have Microsoft Excel and I bet a lot of younger people don’t either. Google Sheets is great because it is accessible from anywhere we log in (laptop, desktop, mobile, etc.) and it’s free to use.

If not, that’s understandable. You’ve already put in so much work to help Canadians everywhere. Thank you for your work!

@Nelson – I have no plans to create any spreadsheets on Google Sheets, but never say never (I only have a finite amount of time to devote to the blog/YouTube channel, so I need allocate it accordingly). I’m glad you’ve been enjoying the site! :)

Hi Justin, can you comment on an acceptable tax-loss pairing for those that have to hold Gold in an Unregistered account? Would something like IAU and GLD work?

@Dwilly – I don’t invest in gold ETFs, so I’ve never used the asset class for tax-loss selling. CRA may take the stance that one ETF that holds gold bars is the same as another ETF that holds gold bars.

Wonderfully comprehensive as always! Thank you!! For those that might have to hold their Gold allocation in an Unregistered account, any suggestions on what would constitute a valid tax-loss harvesting pair? CGL / KILO? CGL/IAU probably not. What about the Horizons ones, HUG?

Hi Justin, what would be the arguments for/against deducting gold from your equity vs. bond allocation? For instance, if I’m aiming for 80 equity / 20 FI generally, what arguments are there for doing 80 equity / 15 FI / 5 gold vs. 75 equity / 20 FI / 5 gold? I know in the examples in this article, you took it out of the equity allocation. But I guess I’m curious because gold has shown to decrease volatility, which is generally the purpose of adding bonds, could there be justification to deduct it from the FI allocation?

OR, using your dataset above (not sure if you looked into this or not), would the reduced standard deviation and the reduced risk adjusted return be eliminated if you had looked at a split of 60 equity / 35 FI / 5 gold instead?

Thanks!

@Amit – Gold is very volatile (just like stocks), whereas bonds are not (so this is the main reason for carving the gold out of the equity allocation). It also led to a higher Sharpe ratio (relative to carving it out of the bond component).

In the comments section of my gold video, I also posted the returns and standard deviation of a 60% stock, 35% bond and 5% gold:

https://www.youtube.com/watch?v=dravkg9j3lk

Awesome, thank you!

Do you have any thoughts on KILO.B from Purpose Investments (MER of 0.25%) or MNT, the Royal Canadian Mint gold reserves ETR (MER of 0.35%)?

@Bjorn – KILO.B would also be a decent gold ETF option. MNT can be a bit tricky – it sometimes sells at a significant premium or discount to its net asset value (so investors need to be cautious when buying and selling).

In your ETF roundup, what do you think of SGOL and/or BAR as compared to IAU?

@AG: SGOL and BAR are also good options for obtaining gold exposure. GLDM is another low-cost option (I chose to compare IAU and GLD as they are currently the most popular ETFs based on AUM).

5% isn’t really worth bothering with. I happen to use a Canadian version of the Golden Butterfly with gold at 20% (good returns but exceptional stability). You need to be fully aware of the benefits and drawbacks though. This approach is more appropriate for high earners who want to store their income safely with decent returns, not for those hoping to get rich in the market. But, if you are buying gold now because its hot, you are buying for the wrong reasons. In that case you should have 0% and just listen to your advisor.