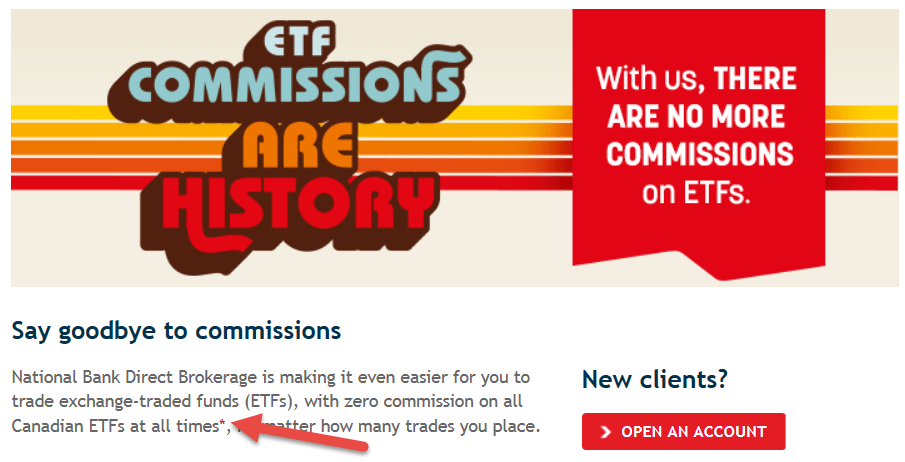

When I first heard that National Bank Direct Brokerage (NBDB) was now offering commission-free trades on all Canadian ETFs, I was impressed. Questrade has been the fan favourite in this low-fee space for awhile now, but their commission-free deal only applied to ETF purchases (not sales).

Source: National Bank Direct Brokerage as of November 24, 2016

After opening an account with NBDB and placing my initial ETF trades, I quickly realized I was still being charged commissions on a number of trades. I reviewed their website again, and noticed a little red star after one of their marketing pitches (see above).

Turns out, you need to buy or sell at least 100 shares of an ETF in order to qualify for their commission-free ETF promotion. This is still a better deal than most of the big banks, but I couldn’t help feeling misled by their advertising.

Avoiding the $9.95 trading commission

As mentioned above, 100 shares of an ETF must be traded in order to qualify for zero commissions. ETFs with higher share prices will require a larger trade size to be eligible for zero commissions. For example, you’ll need to buy or sell over $4,000 worth of the Vanguard U.S. Total Market Index ETF (VUN) in order to avoid the trading commission.

I’ve included the approximate commission-free ETF dollar amounts in the chart below, to help you with your ETF choices.

Approximate Commission-Free Trading Amounts at NBDB

| Asset Class | Security | Commission-Free Account |

|---|---|---|

| Canadian Bonds | iShares Core High Quality Canadian Bond Index ETF (XQB) | $2,122 |

| Canadian Bonds | Vanguard Canadian Aggregate Bond Index ETF (VAB) | $2,618 |

| Canadian Bonds | BMO Aggregate Bond Index ETF (ZAG) | $1,613 |

| Canadian Stocks | iShares Core S&P/TSX Capped Composite Index ETF (XIC) | $2,345 |

| Canadian Stocks | Vanguard FTSE Canada All Cap Index ETF (VCN) | $2,988 |

| Canadian Stocks | BMO s&P/TSX Capped Composite Index ETF (ZCN) | $1,999 |

| US Stocks | shares Core s&P U.S. Total Market Index E?TF (XUU) | $2,190 |

| US Stocks | Vanguard U.S. Total Market Index ETF (VUN) | $4,081 |

| US Stocks | BMO s&P 500 Index ETF (ZSP) | $3,150 |

| International Stocks | iShares Core MSCI EAFE IMI Index ETF (XEF) | $2,646 |

Sources: BMO ETFs, BlackRock Canada, Vanguard Canada as of October 31, 2016

Avoiding the annual administration fee

NBDB also charges $100 plus tax if you don’t invest at least $20,000 with them (so this should be the recommended minimum starting point for any investor).

How to Build an ETF Portfolio at National Bank Direct Brokerage

For those investors who are eager to set-up an ETF portfolio at NBDB, I’ve included a tutorial below that will show you how to get started. In the video you’ll see examples of commission-free ETF trades (as well as the other kind). To reduce the number of trades, consider swapping out VUN, XEF and XEC for the iShares Core MSCI All Country World ex Canada Index ETF (XAW) – this would have resulted in zero-commissions payable for the initial portfolio set-up.

Both US and Canadian ETFs buy and sell commission free at NBDB. Minimum 100 units.

@JL: Correct – since the article was written in November 2016, NBDB now offers $0 commissions on US-listed ETFs as well as Canadian-listed (as long as you purchase at least 100 units).

[…] they began offering commission-free ETF trades, National Bank Direct Brokerage (NBDB) has become the cheapest big bank to invest with (as long as […]

Great post, Justin.

Like you, I, too, was excited when National Bank Discount Brokerage came out with this “big announcement” several months ago. However, I’ve learned not to trust the bold marketing pitches exclusively and quickly read the “terms & conditions” to the offer, namely that 100 units of a given ETF must be traded but also that it applied only to Canadian-listed ETFs. I think this offer still has some value but mainly only in DIY investors looking to switch their higher cost, “actively managed” (I use that term loosely as, in my opinion at least, it probably should be “closet indexed”) mutual funds offered by a “Big 5” bank owned mutual fund dealer subsidiary or from a TD e-Series or Tangerine index mutual fund portfolio into a “basket” of ETFs in that it may offer a commission-free trading opportunity.

For ongoing trading, it’s a relatively useless offer, in my view, unless you might have a multi-million dollar portfolio and are suited to passive investing, in which case, for an extra 50-75 bps, I’d probably look at one of the “robo-advisers” in Canada or even a full-service, multi-channel portfolio manager like PWL Capital. ;)

That said, National Bank Discount Brokerage trading commissions are comparable to RBC Direct Investing, TD Direct Investing or Scotia iTRADE (perhaps even superior to the latter in that one need not maintain $50,000 in assets across all of one’s accounts to qualify for the lower commission tier but, again, for small portfolios of less than that, a robo-adviser or even a TD e-Series or Tangerine index mutual fund portfolio probably makes the most sense in the short- to medium-term). NBDB also has attractive equity research reports (i.e., National Bank Financial Markets, Morningstar and, possibly, S&P Capital IQ). One other downside, however, is supposedly they say they “can’t” link an external bank account from TD Canada Trust or Tangerine Bank but given no reason “why,” saying only interested customers should contact them directly by phone. Hrm? Seems odd as these financial institutions are no different than any other Payments Canada member of the national clearing system.

I’d love for a Canada self-directed discount broker to just go “all in” and offer free buying/selling of either Canadian-listed or Canadian and U.S. listed ETFs in a bid to grow assets under administration, possibly using that as a marketing opportunity to grow their nascent (or currently non-existent) proprietary robo-adviser businesses, transition clients to a full-service investment advisor and also collected the 25 bps “trailer fee” from uninvested cash parked in brokerage accounts and held in nominee form with a major Canadian bank or trust company as well as on regular stock, bond and option contract commissions. They could still have a small “caveat” that the investor must pay any small ECN/clearinghouse/regulatory fees per trade (which are generally pennies) on such ETF purchases/sales, so as not to add any undo cost to the brokerage but the actual “trading cost” to the broker has got to be mere pennies. I’m sure this could be done! :)

Cheers,

Doug M.

Au contraire,NBDB can link to Tangerine, and US ETFs are commission-free.

Hi Justin:

Do you have any plan to make a video for Questrade? Which brokerage you like most out of all brokerages you mentioned? TDDI has a performance tab where investor can see or compare the performance of the account with TSX or S&P 500. Does other brokerages have this option? Thanks!

@WS: I am planning to make various Questrade videos as well. I tend to like RBC Direct Investing, for a number of reasons:

1. Implementing Norbert’s gambit (to cheaply purchase US-listed ETFs in an RRSP account) is extremely easy.

2. You can create performance groups (Modified Dietz) in order to calculate a consolidated rate of return for your portfolio.

3. Good selection of GICs.

Comparing a portfolio’s performance to the TSX or S&P 500 is generally not helpful. An investor should be comparing it to a suitable benchmark (which is likely not either of these indices). I’ll be showing how to do this in future videos as well.

Hi Justin,

Have found DRIP eligibility at RBC DI is very sparse, excluding most BMO & Vanguard ETFs, so if this is important to you, both TD DI and BMO IVL are much more inclusive, though BMO does not DRIP any USD securities.

Have successfully implemented Norbert’s gambit at all three, and RBC does not require an agent’s help (no charge anywhere) to journal the shares to the opposite “side”. Got a nasty interest charge at RBC when I failed to contact them on the journaling, though it was reversed on my contact.

@Davie215: Thank you for the additional DRIP eligibility information. RBC and BMO are definitely the easiest to implement the Norbert’s gambit strategy at, but as you mention, you have to contact them by phone if they end up charging you any debit interest.

If you own a lot of stocks of something like VCN, but you’re not investing quite enough in one go to hit 100 shares, could you sell 100 shares for no commission, then buy say 150 the next day?

@Stevo: Really interesting question. I wouldn’t want to wait a day though, as changes in the ETF price could easily offset the commission savings (you should be able to place the sell and buy trades on the same day). I’ll test it out over the next couple of weeks and let you know how it works out (the downside of the strategy would be the bid-ask spreads, and possible price changes between the trades).

I would be tempted to make the next trade immediately, but worry that NBDB would quickly be on to my shenanigans. I hadn’t thought about the bid-ask spreads. With big ETFs they should be within a few pennies, but on 100 shares that could still be $3-4. Still makes for cheap trades if you prefer dealing with a big bank to someone like Questrade.

@Justin: Did you ever get around to trying this ‘hack’ for avoiding commissions?

@Stevo: Not yet, but I don’t see any reason why it won’t work. I do plan on putting together a video for this. My Norbert’s gambit videos are taking a bit longer than expected.

One thing I’ve sometimes wondered about these bank-owned brokerages is whether I would need to have an account at the parent bank (and pay ridiculous fees there instead of at the brokerage). The brokerage websites don’t usually say… Do you know, by any chance?

Thanks for the ongoing series.

@Tyler: I currently bank with TD, and had no issues setting up and funding the RRSP accounts at the six big bank brokerages for these videos. CIBC Investor’s Edge was a bit of a pain though – they don’t allow you to make contributions using the pay bill function via online banking (if you don’t bank with them), so I had to send them a manual cheque for deposit.

Justin,

Thanks for this. Some questions:

1- Why XAW over VXC?

2- is it not worth trying to buy/sell at least 100 shares to save commissions even if you are a bit out of balance with a given target?

3- and related question: what +/- % boundaries would you put on a given portfolio before re-balancing, again to minimize commissions?

Thanks

@Harold Weil:

1. XAW is slightly more tax-efficient (and cheaper) than VXC: http://www.canadianportfoliomanagerblog.com/war-of-the-worlds-ex-canada/

2. It’s unfortunately impossible to know in advance. If the security you over-weighted has equal performance or outperforms relative to the security that you under-weighted, then this strategy would outperform (and vice-versa).

3. My downloadable calculator uses Larry Swedroe’s 5/25 rule to minimize trading commissions and the realization of capital gains (but similar rebalancing methods would be fine too): http://www.canadianportfoliomanagerblog.com/should-i-rebalance-my-portfolio-now/